Asset-based transportation firms continue to aggressively diversify their businesses, according to the recently completed 2014 TMW Transportation and Logistics Study. Not surprisingly, many view the brokerage/non-asset category as a promising new growth opportunity.

Asset-based transportation firms continue to aggressively diversify their businesses, according to the recently completed 2014 TMW Transportation and Logistics Study. Not surprisingly, many view the brokerage/non-asset category as a promising new growth opportunity.

The results of our latest survey also highlight the improved financial performance enjoyed by many transportation service businesses over the preceding year. Analyzing responses has produced a number of interesting insights into strategies that have been most successful for brokerages and 3PLs as well as blended asset and non-asset business types.

As for businesses that have traditionally employed asset-based operating models, convergence appears to be the operative word. In fact, more than 37 percent of survey respondents already operate multiple business lines and one-third plan to expand into at least one additional category in the next three years. These results reflect the rapidly changing dynamics of the North American transportation market.

The diversification/convergence trend has broad implications for the broker/non-asset sector, both near- and long-term. How will these “new” diversified competitors differentiate themselves from traditional non-asset service providers? How will established brokers and 3PLs adapt to the continued blurring of competitive boundaries with carriers?

Diversification, Profit Potential Align

Our latest study is based on the results of an online survey conducted between July 15 and August 25. Asset-based organizations that participated operate about 87,000 total tractors, more than 173,000 trailers and included 21 of the Transport Topics “Top 100 Carriers.” Non-asset participants included 10 of the Inbound Logistics “Top 50 Third Party Logistics Providers.” Combined revenue for all entities that took part in the study exceeded $24 billion over the preceding 12 months.

In comparison with results reported in our 2013 survey, participants indicated across-the-board gains in key performance indicators across all three sectors covered in the 2014 study—truckload irregular, truckload dedicated and brokerage/non-asset businesses.

For example, respondents to our 2013 survey reported severe margin pressure, with average operating ratio in the mid-90s and just 3.2 percent of participants achieving ORs below 90 percent. Our 2014 results show significant improvement – more than half of respondents achieved an OR of 94 percent or lower and 16.7 percent came in below 90 percent.

Improvement was far from universal, however: While more than half of Truckload Irregular respondents achieved an OR of 94 percent or better, another 39 percent were at 96 or higher, and 5.6 percent of respondents lost money.

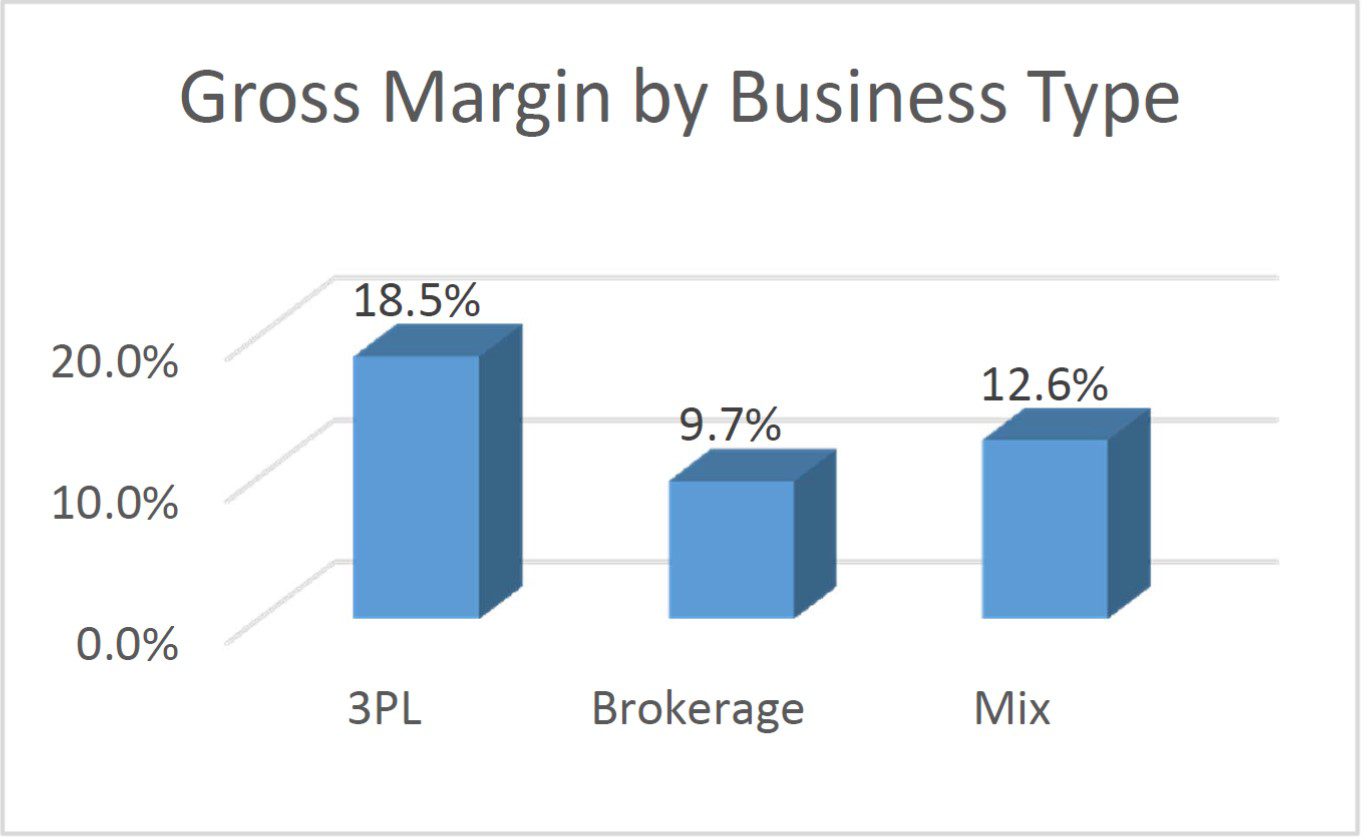

Meanwhile, brokers and 3PLs outperformed their asset-based peers in gross margin at 18.5 and 9.7 percent, respectively, indicating a clear advantage for those non-asset providers that had developed their own carrier networks.

The Loadboard Factor

The use of internet-based loadboards is ubiquitous in the transportation industry, but our study reveals a diminishing role for them in the non-asset space. This is clearly a result of service providers leveraging their TMS solutions to develop and maintain comprehensive carrier networks. For example, 44 percent of responding non-asset firms posted between one-quarter and three-quarters of their freight to loadboards, yet nearly 70 percent of participants actually serviced 25 percent or less of their orders in this manner. Moreover, businesses that relied more heavily on loadboards generally realized lower gross margins than those that depended more heavily on their own carrier networks.

Interestingly, blended broker-carrier organizations accepted much lower percentages of loads offered to them than did pure non-asset providers, yet they earned lower margins overall. 3PLs are therefore leveraging a greater pool of freight opportunities to maximize yield with fewer constraints.

While not altogether surprising, this does point to the need for those entering the non-asset space to invest in technologies that enable them to build and leverage carrier networks as part of their operational strategies. The ability to quickly and efficiently tender loads to network partners requires close monitoring of multiple factors, including insurance expiration dates, safety ratings, capabilities and credentials, lanes, locations, equipment and more. They also will need to develop expanded rating and advanced load planning and execution capabilities that are likely not part of their existing TMS.

Technology, Technology, Technology

The TMW study underscores the fact that the most active participants in the ongoing convergence trend are smaller to mid-size carriers seeking to become comprehensive logistics service providers. As capacity remains tight and competition strong, they recognize the need to address a broadening range of customer needs in order to pursue growth. Key to their success will likely be their willingness and ability to invest in TMS platforms that allow them to operate their diversified businesses more holistically.

Looking ahead to 2015, study participants were prioritizing greater speed and efficiency in processes such as onboarding customers and carriers. Technology is a key enabler here and selecting the right solutions to fit the business is critical.

For logistics business leaders, the findings of the 2014 TMW Transportation and Logistics Study highlight the importance of successful diversification as a near- and long-term growth strategy. As always, thoughtful planning and smart investment in supporting business technology can sharply increase the likelihood of success.

Monica Truelsch is director of marketing for TMW Systems. Monica has contributed to growing market share for advanced technology in diverse sectors, including engineered materials, artificial intelligence and laboratory management. She joined TMW Systems in 2004 as part of the company’s R&D group.

Leave a Reply