In September I began, in February I reflected on, and this week I completed ARC’s Supply Chain Planning Global Market Research Study. I’m going to take this opportunity to summarize some of the study’s key findings.

Supply Chain Complexity Meets Planning Intricacy

Global supply chains continue to be increasingly complex. This is not only due to outsourcing and an ever extending supply chain, but also due to competitive forces such as shorter product lifecycles and a proliferation of SKUs. At the same time, practitioners’ planning processes are becoming more sophisticated. Finally, SCP applications, supported by technology improvements such as data availability and computing capacity, are themselves becoming more sophisticated with more complex and holistic supply chain models, that are being run more frequently, with larger volumes of data representing a more granular level of detail. For example, sales and operations planning (S&OP) was the most frequently mentioned SCP application noted as a sales growth driver during my discussions with SCP vendors. In general, integrated business planning is a process that it a top priority for business executives and this is translating to increased sales of the software solutions that support the process. The pace at which S&OP and rapid analytics is being adopted is reflected in the 15 percent annual growth rate of Kinaxis over the last 3 to 4 years. And SCP suppliers’ plans for it in the future can be seen in SAP’s investment in its Integrated Business Planning for S&OP and HANA. The move to more holistic planning can also be seen in the widespread adoption of multi-echelon inventory optimization (MEIO) and the acquisition of MEIO applications by SCP software suite providers, such as SAP and LLamasoft, to extend their offerings to include this essential capability.

SaaS-a-Fras

SCP applications have been one of the slower supply chain software categories to transition from on-premise, perpetual license sales to the Cloud, or SaaS. But it appears that the transition has reached critical mass. ARC’s research shows SaaS revenues to be the fasted growing segment of the market as newer vendors such as Kinaxis increase market share and larger, more entrenched market participants such as SAP, Oracle, and Infor increase the number of SCP applications they offer in the cloud and transition clients from perpetual license sales to SaaS. However, I want to note that it is still difficult to confidently determine if the transition from perpetual licensing to SaaS with have a net growth effect on the SCP market as a whole. A software company’s revenue typically suffers a setback during this process because perpetual license revenue is recognized upfront, while SaaS revenue is recognized ratably over the subscription periods. As a rule of thumb, it takes approximately 5 years of subscription revenues to equal revenue from a perpetual license. In this sense, SaaS serves as a drag on SCP market growth. However, SaaS also has the effect of transitioning the software supplier’s role to one of an ongoing partnership with customers. This has the potential to extend customer retention and potentially lead to greater long-term revenues for the particular vendor, and potentially increase overall revenues of the market. At the same time, the lower upfront costs reduce barriers to purchase and can encourage small and mid-sized businesses to make the “investment” in the technology, leading to greater market penetration and higher overall revenues for the market.

Summary in a Sentence

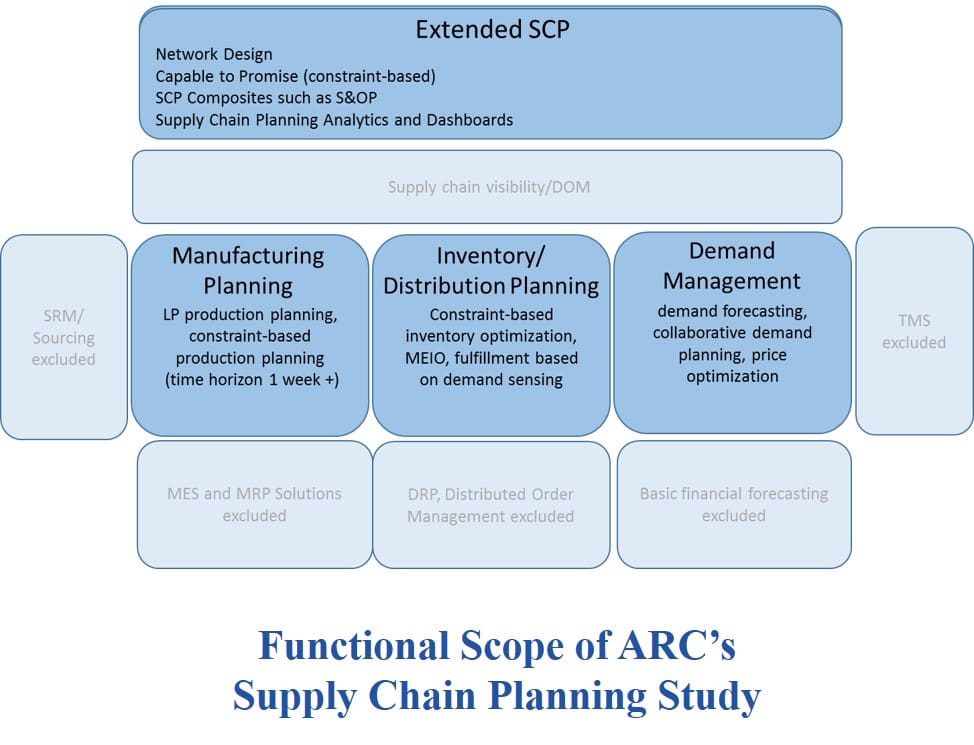

The global SCP market continues to grow, driven by the increased complexity of supply chains, the sophistication of planning processes, and the ability of suppliers to develop and practitioners to adopt more capable, sophisticated, and efficient SCP applications. For more information on ARC’s SCP study; including market segment sizes, market shares of leading suppliers, and growth rates of applications types and sales to end user industries, visit http://www.arcweb.com/market-studies/pages/supply-chain-planning.aspx.

Small and mid-sized businesses need smart and cost effective shipping solutions for seamless business process.

Thank for sharing informative article about technology contribution on supply chain management.

http://www.processweaver.com