In March I provided a brief overview of the global trade management (GTM) solutions market and discussed some of the factors that encourage companies to invest in these solutions. There are a few “independent variables” that can explain GTM sales. Among them are regulation and compliance complexity, regulatory fine risks, supply chain complexity, and tariff costs. Public policy is a major determinant of trade tariffs and regulatory compliance risks. However, trade volumes affect total tariff and duty exposure, all else left constant. At the same time, preferential treatment for some items can amount to substantial cost savings, but also substantial compliance complexity.

In March I provided a brief overview of the global trade management (GTM) solutions market and discussed some of the factors that encourage companies to invest in these solutions. There are a few “independent variables” that can explain GTM sales. Among them are regulation and compliance complexity, regulatory fine risks, supply chain complexity, and tariff costs. Public policy is a major determinant of trade tariffs and regulatory compliance risks. However, trade volumes affect total tariff and duty exposure, all else left constant. At the same time, preferential treatment for some items can amount to substantial cost savings, but also substantial compliance complexity.

Logically enough, there is a strong relationship between GTM sales and the volume (or value) of trade for a product. But this relationship is also dependent upon product complexity. For example, fuels and mining products accounted for 15% of worldwide merchandise trade in 2015. But this category is represented by commodities that do not have a large degree of heterogeneity. Therefore, GTM solutions are not as critical for commodities companies as they are for companies that export/import discrete manufactured items. Discrete items are more likely to require robust item classification capabilities to manage preferential treatment processes. At the same time, supply chain visibility applications are more applicable to steps within the discrete manufacturing process.

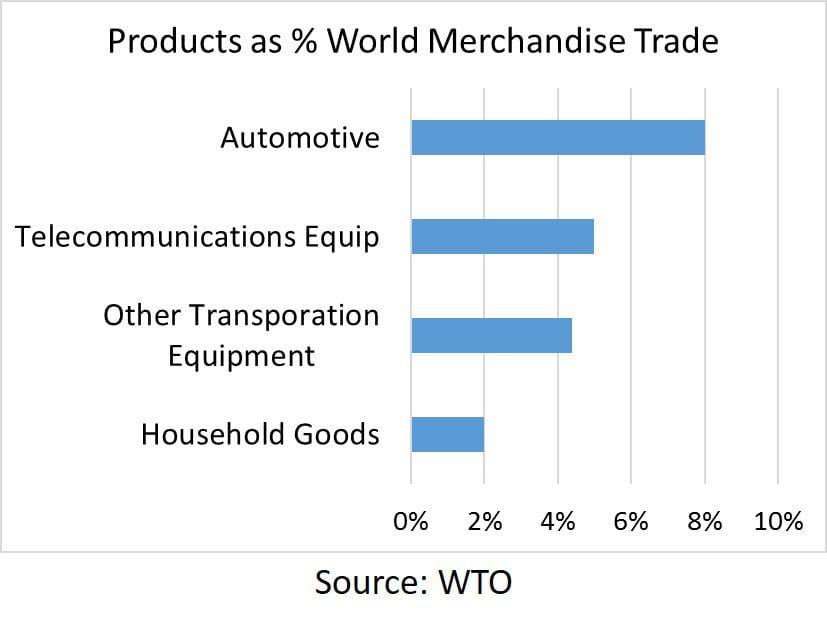

ARC takes into consideration merchandise trade volumes, and trade volume trends, when forecasting the growth of GTM sales. ARC does not forecast GTM sales by merchandise category, but we do break down GTM sales by end-user industry. ARC’s GTM research shows Industrial Machinery, Automotive, Food & Beverage, Electronics, and Household items as leading end-user industries for GTM sales. I reviewed macroeconomic data on merchandise trade of items within those industries as part of a foundation for determining the current state and potential growth rates in trade and GTM sales. Here are a few historical data points on merchandize exports by product category. They show the high growth product categories by region and time frame (source WTO). These categories align well with ARC’s estimates of the industries that adopt GTM solutions to support their global supply chains.

- Worldwide export (value in dollars) of household goods grew by 6% a year between 2010 and 2015. Over the same period, Automotive averaged 4% a year. Telecommunications equipment was the category that experienced the fastest growth in 2015.

- For North American exports, automotive (value in dollars) grew 7% a year between 2010 and 2015, while the other transport category grew by 9% per year. Meanwhile, Pharmaceuticals was the category that experienced the fastest growth in 2015.

- For European exports, automotive (value in dollars) grew 4% a year between 2010 and 2015, as did the other transport category.

- For Asian exports, household goods (value in dollars) grew by 9% a year between 2010 and 2015, while telecom equipment grew by 7% a year.

Overall global trade has been weak by historical standards over the last couple years. In 2015, merchandise trade volumes increased by only 2.6%, compared to rates twice as high prior to the great recession. This weakness in volumes is due to a slowdown in China, falling commodity prices, and exchange rate volatility. Meanwhile, trade as measured in US dollars declined in 2015 due to the sharp appreciation in the dollar. Furthermore, the growth rate of merchandise trade slowed in 2016 to only 1.3%. On a more positive note, the WTO is projecting more robust trade volume growth in 2017 (2.4%) and 2018 (2.1 – 4.0%). The WTO outlook mostly discusses growth factors from a macroeconomic perspective, with further details provided by regions and economic categorization such as emerging markets. However, some other factors are discussed such as government trade policies and reductions in investment spending in the US and China.

Conclusion

Overall it appears that global trade is poised to increase at a rate faster than that of 2016 but slower than the 1.5x GDP rate of the past decade. Ultimately, trade volumes are only moderately important determinants of demand for GTM solutions, as trade regulation and supply chain complexity overshadow the financial effects from trade volumes. In my opinion, macroeconomic uncertainty caused by a lack of political direction in the US and Europe as well as trade imbalances caused by commodity price declines are the major inhibitors to worldwide GDP and trade growth. The lack of political direction is especially detrimental to trade, as major supply chain network decisions tend to be investment decisions that require a long-term perspective.

Next on the GTM research to-do list – ROI of various GTM software functionality and how companies utilize the solutions to drive savings and improve upon internal processes.

With nearly 30% of the world’s gross domestic product currently crossing borders, it is clear that global trade is an integral and growing part of business. The volume of global trade is substantial, and will only increase with time. There are dramatic operational and cash flow benefits to be gained by businesses that implement and execute global trade operations efficiently.

Seems like unless you personally know someone in the global trade operations it will be tuff to break in. Maybe its a case of who you know and not what you. I am hoping at some point my logistics company can divulge into the global operations side.