ARC Advisory Group and DC Velocity magazine have closed our joint survey on the changes logistics operations have experienced in the upheaval of the Covid-19 operating environment in 2020; and the expectations these same executives have about their operating environment in 2021. The goal of this research effort is to capture measurable insights into the rapidly changing fulfillment environment and the direction of change going forward. We are currently compiling and analyzing the response data. In June, DC Velocity will publish an infographic concisely capturing our most significant findings. In the meantime, I looked at a small, but informative subset of respondents – namely the 3PLs. I chose 3PLs because they support a range of industries and very often experience more immediate changes than the facilities of the industries they support, offering a glimpse into broader fulfillment trends.

ARC Advisory Group and DC Velocity magazine have closed our joint survey on the changes logistics operations have experienced in the upheaval of the Covid-19 operating environment in 2020; and the expectations these same executives have about their operating environment in 2021. The goal of this research effort is to capture measurable insights into the rapidly changing fulfillment environment and the direction of change going forward. We are currently compiling and analyzing the response data. In June, DC Velocity will publish an infographic concisely capturing our most significant findings. In the meantime, I looked at a small, but informative subset of respondents – namely the 3PLs. I chose 3PLs because they support a range of industries and very often experience more immediate changes than the facilities of the industries they support, offering a glimpse into broader fulfillment trends.

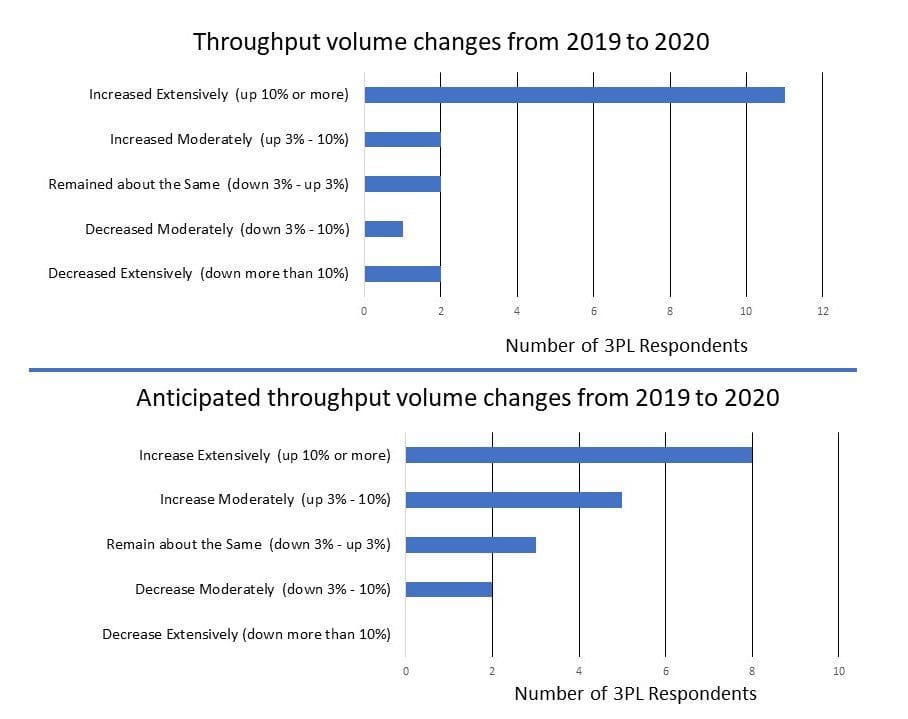

Throughput Volumes

3PLs experienced extensive increases in order throughput volumes in 2020, with the intensity of increases expected to moderate in 2021. As one would expect, direct-to-consumer was the channel that experienced the most extensive (rate of change) and widespread (across respondents) increase in 2020. Like order throughput volumes, the rate of direct-to-consumer increase is expected to moderate in 2021, but the growth in direct-to-consumer is expected to be more widespread (across a larger percentage of 3PLs).

Labor Restrictions

Covid-19 related restrictions caused friction during daily activities and even inertia for many individuals. And this was no different for warehouse operations. Facility-wide labor capacity restrictions appeared to have the most widespread, negative impact on warehouse labor operations in 2020. Although general social distancing and quarantine driven labor unavailability also caused notable difficulties. Looking forward through 2021, 3PL expectations are that these Covid-19 related labor restrictions will still have some impacts, but less substantial than those experienced in 2020. How did 3PLs respond to minimize the impacts from Covid-19 restrictions? Warehouse process changes and facility layout changes were the most frequently utilized tactics that proved effective at regaining productivity.

Technology Solutions

In the longer term, it is likely that technology investments will play a role in minimizing the risk associated with a pandemic or similar impediment to warehouse productivity. To better understand warehouse investment priorities for the next three years, we asked respondents to select the one warehouse technology investment that is of highest priority to their organization. WMS and warehouse labor management applications were noted, as would be expected. However, somewhat surprisingly, item picking and case picking robotics were also noted. Generally speaking, 3PLs have been risk averse with respect to long payback automation investments due to limited contract durations and the likelihood of differing fulfillment requirements as clients change. But I view picking automation adoption as an indication that 3PLs are accepting greater investment risk to reduce the variable costs of fulfillment in their contract relationships.

Be sure to view the infographic displaying our research findings in the June issue of DC Velocity Magazine, and in future Logistics Viewpoints articles.