I am placing the finishing touches on ARC Advisory Group’s research on the warehouse management systems (WMS) market (https://www.arcweb.com/market-analysis/warehouse-management-systems). ARC has been publishing structured research on the global WMS market for over 20 years and this history provides us with valuable context for understanding the changes that occur and serves as an anchor to our five-year market forecast.

I am placing the finishing touches on ARC Advisory Group’s research on the warehouse management systems (WMS) market (https://www.arcweb.com/market-analysis/warehouse-management-systems). ARC has been publishing structured research on the global WMS market for over 20 years and this history provides us with valuable context for understanding the changes that occur and serves as an anchor to our five-year market forecast.

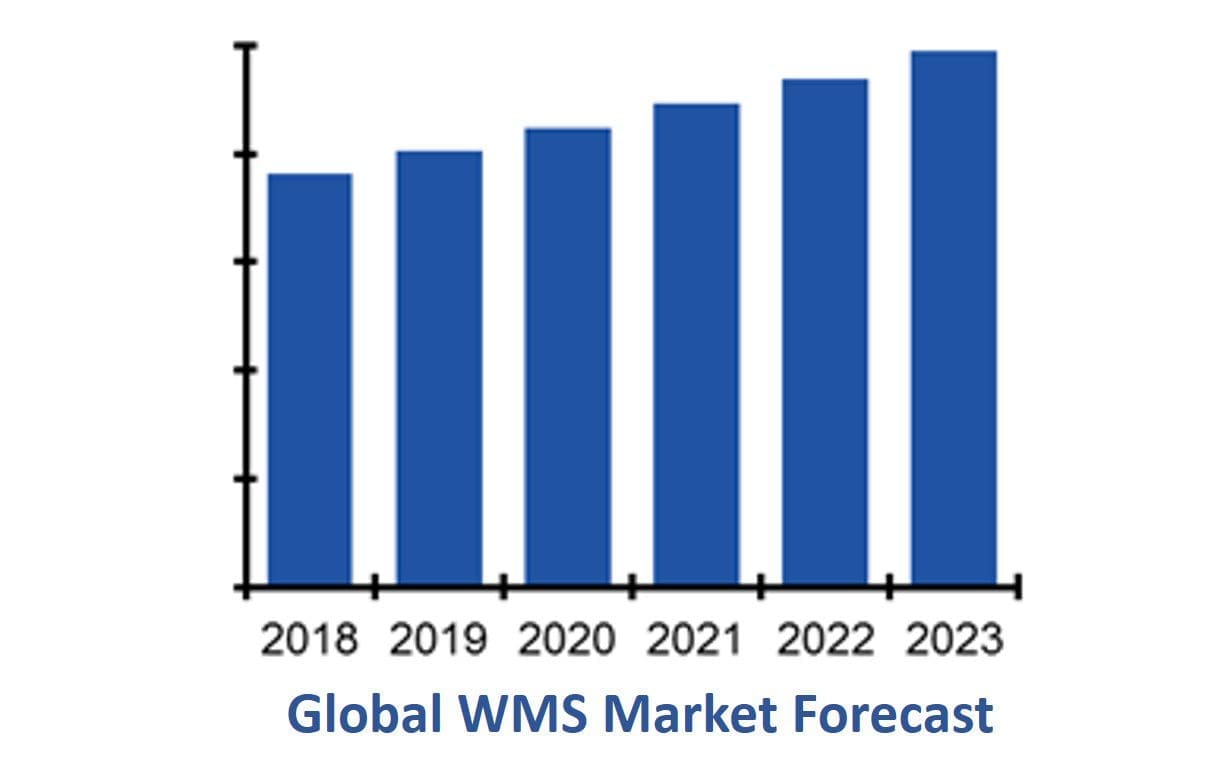

The WMS market continued its persistent growth in 2022. Although the growth is obscured by some technicalities. In fact, I chose the metaphor of growth “beyond a reasonable doubt” to reflect the burden, or headwinds, that WMS sales had to overcome to achieve growth in 2022. First, ARC Advisory Group uses the US dollar as the base currency for its market research (we offer the ability to easily translate to various currencies, but I digress). The value of the euro declined by almost 11 percent in 2022. This effectively means that 10 percent growth in euros translates to a 1 percent decline in dollars. This effect was even more pronounced for revenues translated from Japanese yen (a 15 percent decline).

Secondly, the WMS market continues its shift from a perpetual licensing model to a software-as-a-service subscription model. A subscription model reduces upfront costs to customers, but it also reduces upfront revenues for suppliers. The delayed recognition of revenue, at least temporarily, inhibits the growth of the market and potentially reduces the size of the market until critical subscription mass is reached. Although some suppliers have transitioned a large percentage of customers to SaaS, most WMS suppliers have not yet reached “critical subscription mass.” Even with both of these headwinds, the WMS market grew by middle single digits in 2022, as measured in US dollars. I believe it is fair to say that growth in constant currencies was around 10 percent.

Change and Evolution in 2022

There were many ownership changes and rebranding activities that occurred in 2022 and early 2023. 3PL Central rebranded as Extensiv in 2022. The former AFS Technologies is now branded as Exceedra by TELUS and is part of TELUS Consumer Goods. Generix Group went private in a buyout by private investors and management. Toyota Industries acquired viastore in the summer of 2022. Made4net acquired Zethcon in 2022 and was subsequently acquired by the Ingka Group (IKEA) in 2023. Finally, in early 2023, Hardis Group acquired Sislog, the Spanish warehouse management software (WMS) division of Atos.

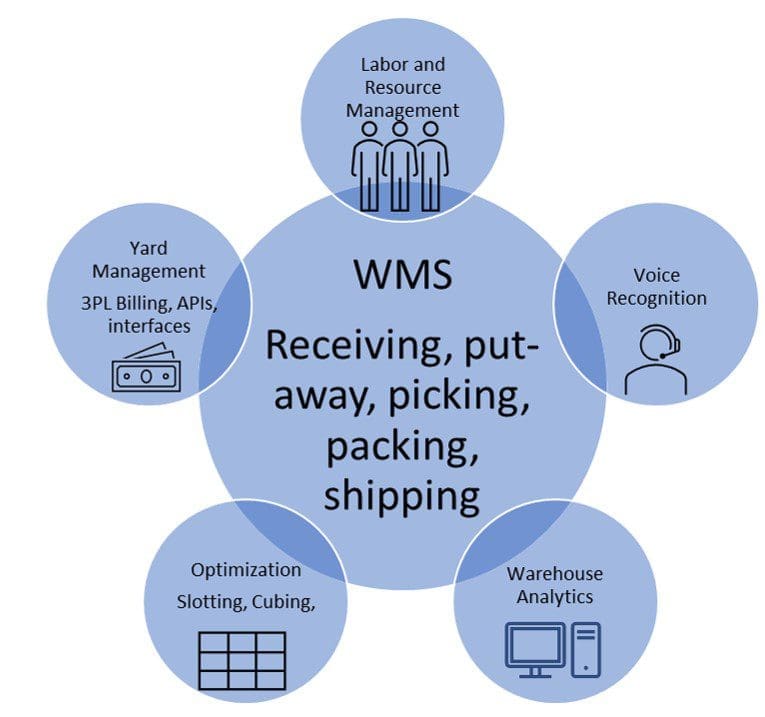

In 2022, the WMS market continued its shift from perpetual licensing to SaaS licensing, with the SaaS revenue type being one of the market’s fastest growing segments. WMS suppliers indicated that their users continued to operate within tight labor markets and with a shortage of reliable workers. As a result, technologies and capabilities that drive productivity were in high demand. WMS functionality such as labor management and resource management were highly important. Also of interest was integration with complementary technologies such as warehouse automation and robotics. Modern APIs, pre-built connectors, and warehouse analytics were all noted as valuable capabilities. Additionally, providers with a WCS/WES considered it an important characteristic of their offering.

2023 and Beyond

The major factors contributing to market growth remain in effect. E-Commerce fulfillment and Omni-Channel operations are the most pervasive trends contributing to WMS sales. Most notably, demand from grocery is especially strong. Furthermore, WMS suppliers continue to invest in their technology platforms and the ability to easily integrate among WMS functions and with those adjacent to warehouse processes, including transportation management, order management, warehouse automation, and robotics. For those interested in the research, I expect it to be available for purchase in August. Please reach out to your account manager for more information, or contact the author at creiser@arcweb.com.