The first two weeks of August is peak vacation season. Many of us are away with friends and family. But those of us in the office this week are also likely planning for the second half of the year. It seems that everyone hits the ground running in the first week of September. So I thought I would take this opportunity to summarize 2017 year-to-date economic data most pertinent to the logistics industry. This data provides a timely snapshot of the industry’s performance for the first half of the year. Logistics professionals can use this data to inform their views and assumptions about the status of the industry and its likely path going forward.

Summary

Summary

US GDP grew at about a 2 percent annual growth rate in the first half of the year. The logistics and warehousing industry grew at a tepid rate in the first quarter. But this is positive when compared with the Q1 performance of recent years when the industry actually contracted, likely due to atypical seasonality. Also, the industry appears to be growing at a healthier rate when taking leading indications from the ISM PMI into consideration. International trade volumes have increased substantially from 2016. The value of NAFTA trade increased by about 6 percent year-over-year in the first five months of the year, although a portion of the value increase is a result of crude oil price increases. Vehicles and automotive parts remains the largest commodity group that the US trades with both Canada and Mexico.

Logistics Activity in the First Half of 2017

US Real GDP increased at an annual rate of 2.6 percent in the second quarter and 1.2 percent in the first quarter. Similar to GDP, data from economic indicators that more closely reflect logistics activity support the view that the year started off slow for the logistics industry, but accelerated through the remainder of the first half of the year.

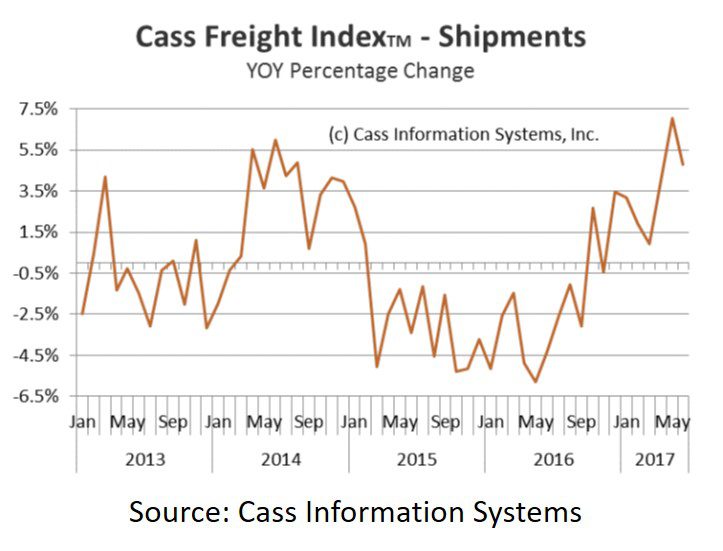

The Bureau of Economic Analysis reported that Transportation and Warehousing increased 0.4% in Q1. This is actually strong performance when compared to Q1 data from 2015 and 2016 (Q1 2016 was -6.7% and Q1 2015 was -9.5%). The US DOT Freight Transportation Services Index (measures the output of the for-hire freight transportation industry and consists of data from for-hire trucking, rail, inland waterways, pipelines and air freight) grew by 1.4 percent in the second quarter, following a 0.5 percent decline in the first quarter of 2017. However, the Q1 decline is a quarter to quarter change that appears to reflect seasonality, as well. The ISM Non-Manufacturing Report On Business reported that the Transportation & Logistics industry contracted in January, but then grew each month from February through June. Finally, the Cass Freight Index registered year-over-year shipment volume increases for each of the first six months of the year. Sequentially, June is the only month that registered a decline (-0.4 percent).

International Trade in the First Half of 2017

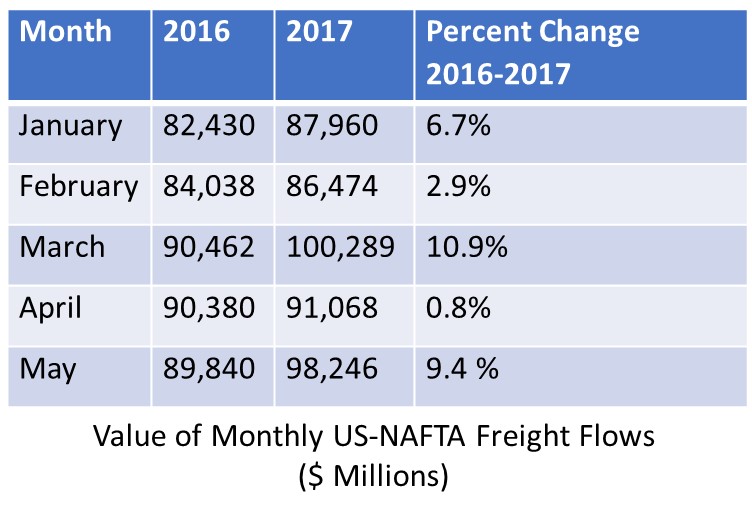

According to US Census data, US exports in the first half of 2017 totaled $763.6 billion, representing a 7.3 percent increase over the total for the first half of 2016. Export data is compiled from the Electronic Export Information (EEI). Imports for the first half of 2017 totaled $1.158 trillion, representing a 7.5 percent increase over the first half of 2016. Data on imports is compiled from US Customs ACS. For the first five months of the year, Canada, China, and Mexico were the three leading trade partners of the  US, each representing approximately 15 percent of US trade. Japan and Germany followed, with about 5 percent each. US-NAFTA freight flows for the first five months of 2017 totaled $464 billion, representing a 6 percent increase over the same period in 2016. In May, the value of commodities moving by all modes increased, with pipeline and vessel increasing the most due to increased mineral fuel prices and trade volumes. In May, vehicles and parts was the top commodity category that the US traded with Canada, as well as with Mexico.

US, each representing approximately 15 percent of US trade. Japan and Germany followed, with about 5 percent each. US-NAFTA freight flows for the first five months of 2017 totaled $464 billion, representing a 6 percent increase over the same period in 2016. In May, the value of commodities moving by all modes increased, with pipeline and vessel increasing the most due to increased mineral fuel prices and trade volumes. In May, vehicles and parts was the top commodity category that the US traded with Canada, as well as with Mexico.

Final Word

The logistics industry experienced growth in the first half of 2017, with more robust growth occurring in the second quarter. This trend is consistent with US GDP growth; however, it is also subject to greater seasonality than the economy as a whole. Data from the first half of 2017 point to consistent levels of growth going into the second half of the year.

{kind=link}

Leave a Reply