I’m currently updating ARC Advisory Group’s research on the global warehouse automation & control systems market. I have compiled and analyzed the data for 2018 and just began writing the final report. This blog post will provide some high-level insights that I have obtained at this point in the process.

For starters, the 2018 growth of the global warehouse automation market was a full 2 percent greater than my prior year’s forecast had projected. Last year I stated that the 2017 growth rate was unsustainably strong. I considered it unsustainable due to the human resource constraints that many automation systems providers were experiencing. Of course, a tight labor market isn’t the worst problem to encounter, but it can hinder growth. Implementation and consulting labor continued to impede the market’s growth in 2018. In fact, “a lack of qualified employees” was the most frequently mentioned market growth inhibitor during my discussions with warehouse automation suppliers. However, 2018 growth was strong and order backlogs are in place to support comparable growth in 2019.

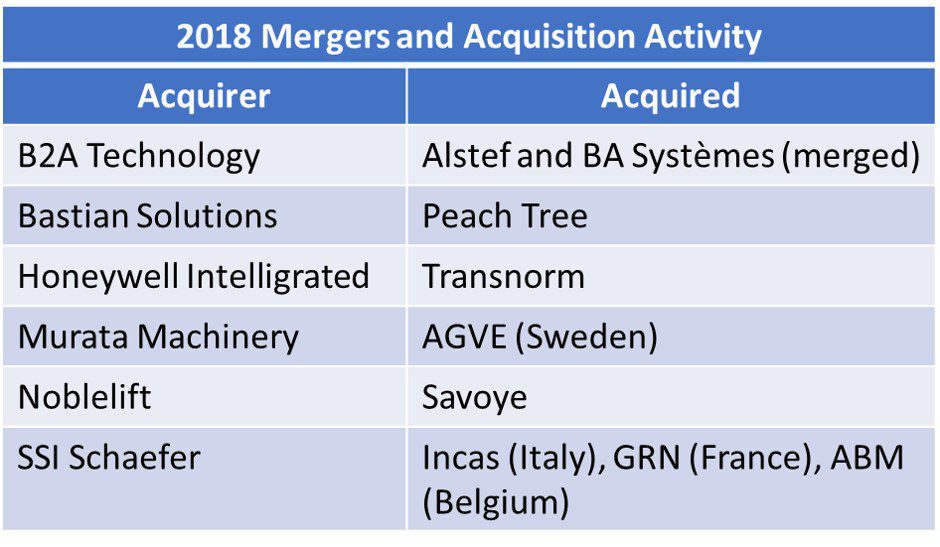

Mergers & Acquisitions

There weren’t any “big bang” acquisitions (like KION’s acquisition of Dematic in 2016), but there were a number of transactions that expanded the acquirer’s solution set or geographic presence. For example, the merger of Alstef and BA Systèmes combined Alstef’s stacker crane and other pallet handling solutions with the AGV and robotics capabilities of BA Systèmes. Similarly, Murata Machinery’s acquisition of AGVE provided the company with immediate access to AGV capacity and capabilities. Honeywell intelligrated’s acquisition of Transnorm expands its presence in Europe and extends its portfolio of conveyor and sortation solutions. SSI Schaefer’s acquisitions expand the company’s offerings and presence in Italy (Incas), France (GRN), and Belgium (ABM). Similarly, the Chinese firm Noblelift obtained a European presence and a complementary, high-growth solution set from its acquisition of Savoye.

There weren’t any “big bang” acquisitions (like KION’s acquisition of Dematic in 2016), but there were a number of transactions that expanded the acquirer’s solution set or geographic presence. For example, the merger of Alstef and BA Systèmes combined Alstef’s stacker crane and other pallet handling solutions with the AGV and robotics capabilities of BA Systèmes. Similarly, Murata Machinery’s acquisition of AGVE provided the company with immediate access to AGV capacity and capabilities. Honeywell intelligrated’s acquisition of Transnorm expands its presence in Europe and extends its portfolio of conveyor and sortation solutions. SSI Schaefer’s acquisitions expand the company’s offerings and presence in Italy (Incas), France (GRN), and Belgium (ABM). Similarly, the Chinese firm Noblelift obtained a European presence and a complementary, high-growth solution set from its acquisition of Savoye.

The Obligatory E-Commerce Statement

This year’s research on the warehouse automation market shows (once again) that the fulfillment requirements from the ongoing, widespread growth in e-commerce continues to be the most prevalent factor stimulating growth in demand for warehouse automation and control systems. Some of the notable, publicly stated information includes KION’s statement that 47 percent of 2018 Supply Chain Solution’s (Dematic) revenues were from pure play e-commerce players (fiscal year 2018 update call); and Honeywell Intelligrated’s mention of its project at Amazon’s 600,000 square foot warehouse near Calgary, Canada (earnings presentation).

Although the trend of warehouse investment spending in support of e-commerce is not new, there is a “shift” in the demand patterns – namely by type of retailer. Most pronounced is the spike in demand for systems by the grocery segment. This spike is visible in the WMS market as well. But is it substantially stronger in the warehouse automation market. A large percentage of warehouse automation providers mentioned grocery as a high growth vertical for 2018 and into the near future. In addition, there has been product development focused on systems that can deliver productivity gains to grocery operations. For example, Vanderlande recently launched Fast Pick, its 2D shuttle system that offers greater throughput and built-in sequencing, removing the requirement for conveyor loops. In addition, AutoStore recently launched Black Line, a new line of AutoStore designed for high-throughput. This solution could be a good fit for grocery and it will be interesting to see if AutoStore’s success will continue with Black Line, and the degree to which it will penetrate the online grocery segment.

Final Word

I expect to complete ARC’s Warehouse Automation & Control market research within the month and it should be published before the end of June. Please reach out to your account manager if you are interested in learning more about this high-growth market.