ARC Advisory Group released its updated Warehouse Automation & Control (WAC) market study last week. This research is an evaluation of the market with detailed analysis of the 2017 base year and a five-year forecast through 2022. I would like to take this opportunity to communicate some of the prominent themes I observed during the research process.

ARC Advisory Group released its updated Warehouse Automation & Control (WAC) market study last week. This research is an evaluation of the market with detailed analysis of the 2017 base year and a five-year forecast through 2022. I would like to take this opportunity to communicate some of the prominent themes I observed during the research process.

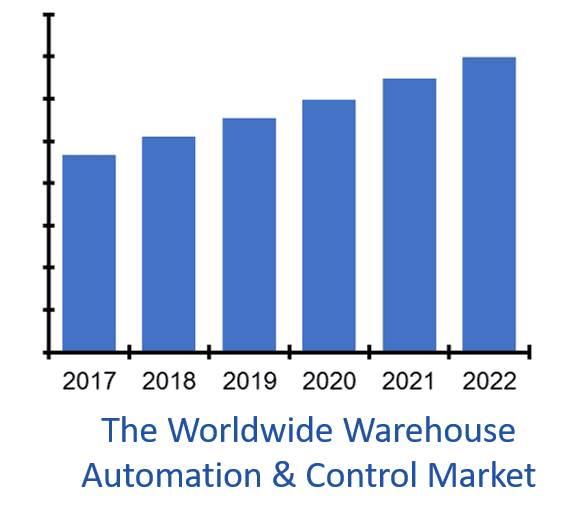

2017 – A Stellar Year

The market’s growth in 2017 was substantially greater than I had expected. In fact, I consider the 2017 growth rate to be unsustainably high, as many providers (especially those in Europe) noted that they are having difficulties finding enough qualified employees to handle their prospective project growth. Similarly, 2017 was an especially strong year for the global economy, as measured by the International Monetary Fund (IMF). I do believe the warehouse automation investments are affected by the macroeconomic environment. However, I don’t believe they are currently subject to the same level of cyclicality as most capital expenditures. This is due to the fact that a large percentage of warehouse automation investments is driven by the secular change in fulfillment operations, namely the transition from tradition brick and mortar retail to e-commerce fulfillment. And it turns out that the shift to e-commerce is happening at a faster pace than many retailers and warehouse automation providers had imagined just a couple years ago. In fact, annual e-commerce sales in the US have doubled over the last five years. On top of e-commerce growth, customers have come to expect fast delivery of goods ordered online. These next day delivery expectations have made agility a primary requirement of today’s warehouses, and this requires different capabilities than the high-throughput waving operations of the past.

Warehouse Automation Capabilities in Demand

System adaptability and scalability are top priorities for today’s warehouse automation projects. This is being achieved through greater software intelligence in warehouse control systems, layout of subsystems in the warehouse, and within subsystems themselves. Equipment subsystems in high demand include shuttle systems, high-density storage, pocket sorters, AGVs, and traditional conveyor and sortation systems. Warehouse automation vendors are expanding and improving upon their control and material flow systems with new optimization algorithms and real-time monitoring and response capabilities that proactively avoid bottlenecks. Shuttle systems remain at the top of the list due to their scalability and strong fit for e-commerce fulfillment. Shuttle systems are also being used for production logistics, as are AGVs as Steve Banker described earlier this week. (The industrial manufacturing and automotive industries have shown increased demand for warehouse automation systems, adding to the e-commerce driven demand wave). Meanwhile, the emerging category of collaborative autonomous mobile robotics (AMR) continues to evolve rapidly. Although adoption is still limited, these solutions show great potential and I expect an adoption inflection point in the near future. It’s also worth noting that the most sophisticated guided vehicle system isn’t always the best solution for a given business case. As Steve noted in his article about AGVs for assembly lines, “it can be counterproductive to pay extra for a form of intelligence or autonomy not needed to complete a particular kind of task.” This is also the case for AGVs in warehouse fulfillment operations. For example, SSI Schaefer offers an AGV branded the WEASEL. It is a cost-effective option that is scalable and a good fit for certain requirements.

Mergers & Acquisitions to Continue?

There have been a number of acquisitions within the WAC market over the last few years, although the pace decreased recently. The most prominent acquisitions in 2017 were Toyota Industries’ acquisitions of Bastian Solutions and Vanderlande. Perhaps more significantly, 2017 was a year of business integration for prior years’ acquisitions. Honeywell integrated Intelligrated into its Safety and Productivity Solutions business unit, and KION integrated Dematic and Egemin into its Supply Chain Solutions segment. Notably, both KION and Toyota Industries are leading providers of industrial trucks and forklifts – a complementary market to WAC systems. I expect acquisitions of WAC providers by large industrial companies to continue in the near future, but at a measured pace. The market continues to offer the opportunity for increased growth to diversified industrial companies. However, the number of viable acquisition candidates has diminished due to the recent acquisition activity.

For further information on the content and structure of ARC’s research on the global warehouse automation & control market, contact creiser@arcweb.com or your ARC Advisory Group account representative.

Leave a Reply