On Saturday I engaged in a rare weekend activity for myself – I actually thought about supply chain. I thought about the transition from “push” processes to greater use of demand pull in replenishment; how retailers are sharing downstream POS data with their suppliers to develop a more efficient supply network; how multi-echelon inventory optimization is now widely adopted; and how lean manufacturing and inventory management practices have evolved. In general, I was thinking about the vast improvements in supply chain processes and technologies over the last 25 years.

Source Wikipedia

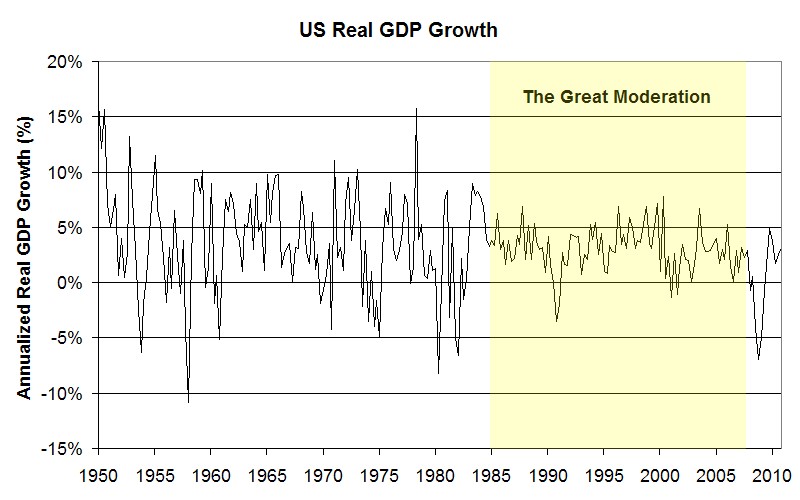

Shortly thereafter, I stumbled upon a reference to a concept that Economists refer to as The Great Moderation. The moderation refers to a major decrease in the volatility of economic growth beginning sometime in the 1980s. This concept spread to the mainstream when former Federal Reserve Chairman, Ben Bernanke, gave an often quoted speech on the subject. My recollection of the speech was that Bernanke attributed the moderation to improvements in monetary policy. But wait! I thought. I know that inventory is a volatile segment of the US economy, and production and inventory management practices made great strides at about the same time as the great moderation. We talk about the positive corporate benefits of supply chain improvements, but is it possible that this major increase in macroeconomic stability was driven not by monetary policy but by the improvements in supply chain? Or was I way off base to even consider the connection?

Well, after doing some additional research, the answers to my self-imposed questions are “Yes, partially; and No.” I re-read the transcript from the Bernanke speech and the following line is included toward the beginning of the article:

“Some economists have argued, for example, that improved management of business inventories, made possible by advances in computation and communication, has reduced the amplitude of fluctuations in inventory stocks, which in earlier decades played an important role in cyclical fluctuations.”

I like that some economists are crediting productivity (often termed “structural changes”) rather than focusing exclusively on monetary policy. What did these economists have to say? Well, in 2000 McConnell and Perez Quiros noted that the ratio of inventory to sales of durable goods has been declining steadily since the 1980s. They state the following:

”One hypothesis is that changes in inventory management, such as the use of `just-in-time’ techniques, have brought about the reduced share of durables inventory and the associated stability of aggregate output.“

In support of this hypothesis, they also referenced a concurrent increase in the proportion of PMI survey respondents ordering production materials with short lead times (15 days or less or 30 days or less).

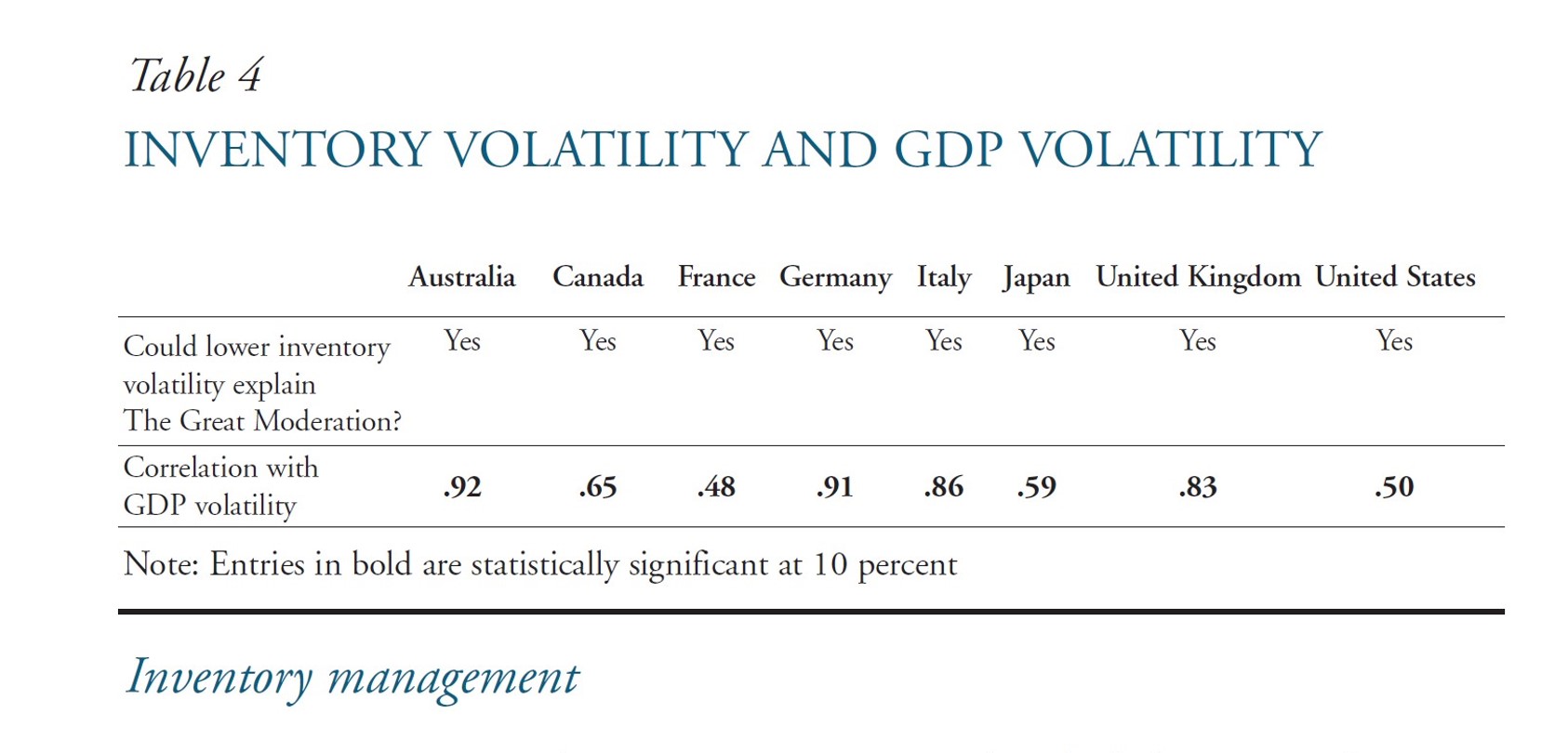

A paper written by Peter Summers and published by the Kansas City Fed discusses the potential causes of the great moderation and analyzes data across countries. He concludes that decreases in GDP volatility exist internationally and suggests that improved monetary policy and improvements in inventory management techniques may have contributed to the Great Moderation. He supports this suggestion with a chart that shows eight major economies of the world where inventory volatility and GDP volatility show statistically significant correlation.

Source: Peter Summers, Kansas City Fed

So give yourselves credit a pat on the back. Although we at Logistics Viewpoints often write about the organizational benefits and efficiency gains from supply chain investments, it appears that your efforts are also contributing to the macroeconomic stability of nations across the globe!

I think the cause of the reduction in economic volatility is much more direct and obvious. Manufacturing bares the major brunt of most recessions and booms during recoveries. Manufacturing’s share of GDP is off about as much as the volatilty % has been reduced. At the same time government’s stable share has risen. Conclusion: less volatility!

Hello Harry. Thank you for your comment. At first I thought that the shift in the US economy away from manufacturing and toward services may have been a major factor as well. However, I do not believe that is the case. The Great Moderation is about volatility, or variation around the mean. The reduction in US production explains the reduction of absolute durable goods manufacturing, but not the volatility around that growth rate (reduction). McConnell and Perez Quiros, referenced and linked in my post above, addresses your supposition and on page 18 they state, “…From this we conclude that changes in the composition of output, and the corresponding breaks in the growth contributions of structures and nondurables, are not sufficient to explain the reduction in aggregate volatility in the early 1980’s.” I’ll leave the regression analysis to the economists. But please let me know of a peer reviewed research paper that supports your perspective. It would be interesting to review.