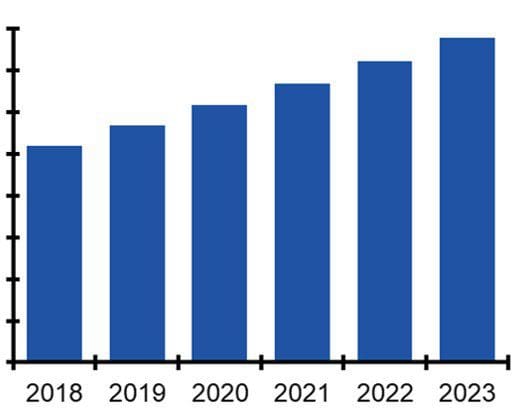

I am happy to report that I have completed and published ARC Advisory Group’s Warehouse Automation & Control (WAC) market study. This research is an evaluation of the market with detailed analysis of the 2018 base year and a five-year forecast through 2023. I would like to take this opportunity to communicate some findings from the research and the following perspective on the market that I have established as a result: The warehouse automation market currently exhibits many characteristics that lead me to believe the competitive landscape is on the verge of rapid change. This isn’t typically the case with a mature market. But e-commerce growth, robotics advancements, and international competition have set the stage for an acceleration of change. Market participants that remain complacent are likely to suffer as a result.

I am happy to report that I have completed and published ARC Advisory Group’s Warehouse Automation & Control (WAC) market study. This research is an evaluation of the market with detailed analysis of the 2018 base year and a five-year forecast through 2023. I would like to take this opportunity to communicate some findings from the research and the following perspective on the market that I have established as a result: The warehouse automation market currently exhibits many characteristics that lead me to believe the competitive landscape is on the verge of rapid change. This isn’t typically the case with a mature market. But e-commerce growth, robotics advancements, and international competition have set the stage for an acceleration of change. Market participants that remain complacent are likely to suffer as a result.

The Three As – Acquisitions, Asia, and AGVs

Warehouse Automation Acquisitions and Asia

Last month, in Status Update: Warehouse Automation Market, I stated that there were not any “big bang” acquisitions in 2018, but there were a number of transactions that expanded the acquirer’s solution set or geographic presence. Most notably, the Chinese firm Noblelift acquired the French firm Savoye. Prior to 2018, there were a number of large international acquisitions including Toyota Industries’ acquisitions of Vanderlande (Netherlands) and Bastian Solutions (US), KION’s acquisition of Dematic (US), and Midea’s (China) acquisition of Swisslog (KUKA). These acquisitions highlight the degree to which large industrial companies with abundant financial resources and established distribution channels are acquiring warehouse automation providers, partially due to the high growth rate of the industry. There is also a notable trend for these acquisitions to establish an international presence for the acquirer. Finally, Chinese and Japanese companies represent a large percentage of the acquiring firms, and overall capital deployed. This is a fairly recent trend.

Asia and AGVs

Did you attend ProMat or LogiMAT this year? I attended ProMat and there was a notable increase in Asia headquartered warehouse automation providers exhibiting at the show, including GreyOrange. GreyOrange, in particular, has established itself internationally with some substantial orders, including XPO Logistics in the US and Zalando in Europe. Also, Chinese AGV providers such as Quicktron and Geek+ have thousands of units deployed at warehouses in China, and Siasun’s overall warehouse automation installed base is substantial. This information leads me to believe that warehouse automation is more well-established in China than I previously believed, and that these providers, along with GreyOrange, warrant competitive consideration by the Western European and North American providers. Simply put, they represent emerging competition.

The Market, Macroeconomics, and Driving Forces

Product development is occurring at a rapid pace within the warehouse automation market, however technology diffusion may be occurring more rapidly. Geographic expansions and capital investments are occurring across numerous paths. However, there are a number of paths that are new, not the well-traveled routes of the past. I believe the rate of change in the market landscape is poised to accelerate. I believe these trends are driven by a few pervasive factors: the high growth rate of the market, high levels of investment and rapid technology diffusion, and massive current account/capital account imbalances between nations. After all, a trade deficit implies a capital account surplus, which is another way of saying that China and Japan have a lot of dollars they can use to purchase US assets. It appears that warehouse automation companies are on their radar. This is not a positive or a negative, just an economic factor. I believe it is wise for warehouse automation suppliers to view their competition broadly.