The phrases “transitory inflation” and “supply chain disruption” have been frequently used in the general and business news media this summer. And they have at times been used together to describe the general economic environment. Certainly, supply chain constraints are a partial cause of the current above trend inflation. Furthermore, there is much discussion about the word “transitory,” as used by Federal Reserve Chairman Jerome Powell to describe what he believes is like a short-term phase of price increases. Nonetheless, it is interesting that the discussion has evolved from possible inflation to whether or not it is transitory or longer-term. Also, it is interesting that supply chain is at the center of the discussion, rather than oil prices or monetary expansion as has been the case when past inflationary periods are discussed. Let’s look at some publicly available information on the topic/s.

Whitehouse Council of Economic Advisors

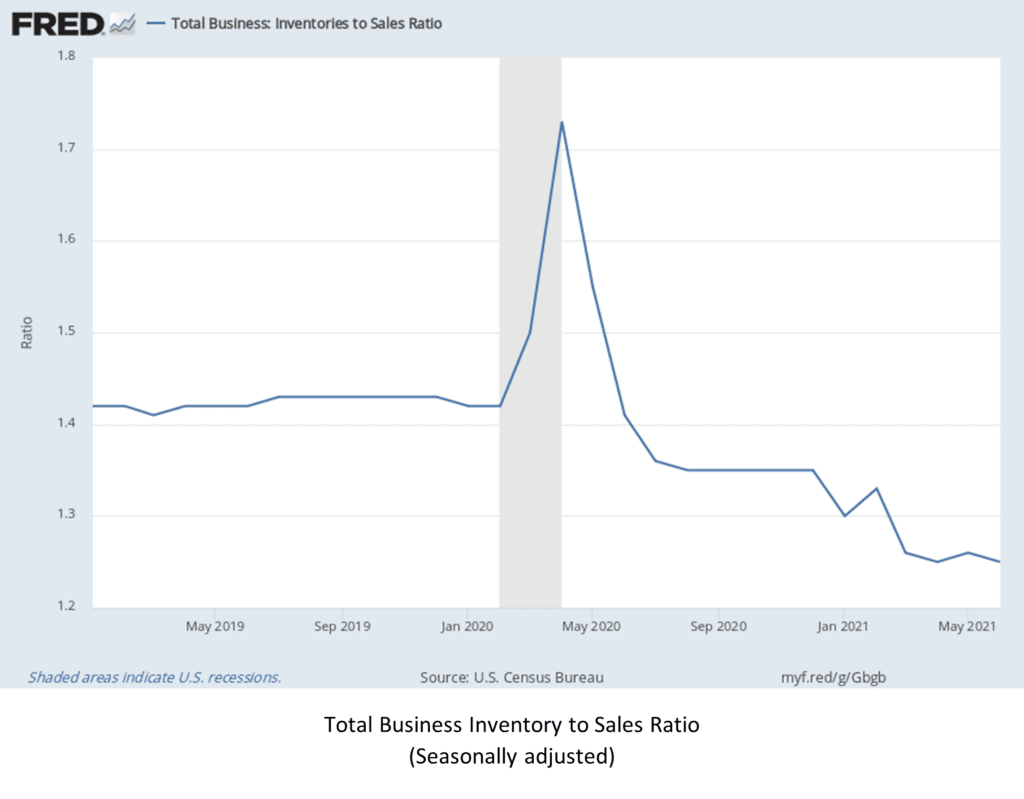

Look no further that the blog of the Whitehouse Council of Economic Advisors for commentary on the connection between supply chains and inflation. A post from June discusses how the pandemic has disrupted supply chains focuses on the rapid deceleration and subsequent acceleration of economic activity and the friction of getting back up to speed. Supply shortages, low inventory to sales ratios, and hiring lags are noted as factors at play. Data as recent as the end of June 2021 show that inventories remain below 1.3 times a month’s sales, a low for the period since January 2019 included in the chart.

In a subsequent Whitehouse.gov blog post, titled ”Historical Parallels to Today’s Inflationary Episode” the authors’ conclusion stated, “No single historical episode is a perfect template for current events. But when looking for historical parallels, it is useful to concentrate on inflationary episodes that contained supply chain disruptions and a spike in consumer demand after a period of temporary suppression.” With that said, let’s take a look at some recent and more granular data on sales, prices, and supply chain performance.

This Summer’s Sales, Prices, and Supply Chain Performance

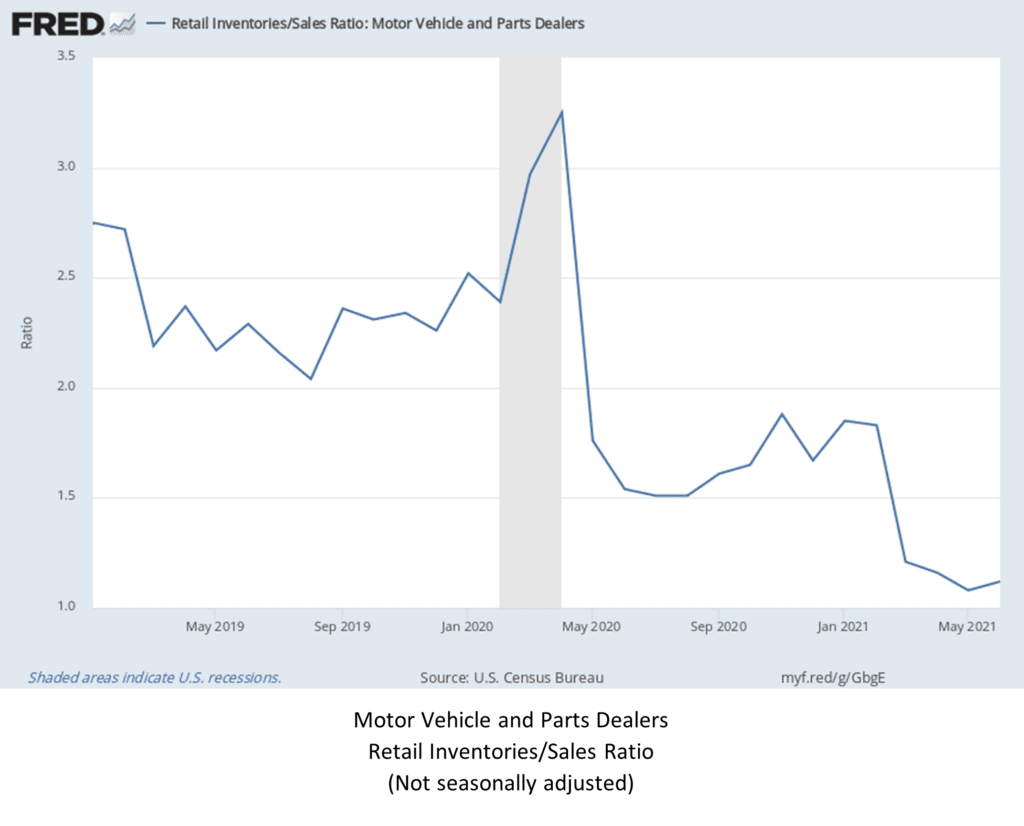

Yesterday, the U.S. Census Bureau announced the advance monthly sales for retail and food services sales for July. The estimate of $617.7 billion represented a decrease of 1.1 percent from the previous month (June), but a 15.8 percent increase from July of 2020. So, the month-to-month change indicates a recent slowing in the longer trend of year-over-year business activity growth. By kind of business, the notable month-to-month slowdowns were motor vehicle parts and dealers (-3.9%), clothing and clothing accessory stores (-2.6%), and non-store retailers (e-commerce) (-3.1%).

Last week, the Bureau of Labor Statistics released the Consumer Price Index (CPI) for July. It stated that the items index increased 5.4 percent over the last 12 months, before seasonal adjustment. Meanwhile, all items, less food and energy (aka “core inflation”) was up 4.3 percent. These price increases are clearly above the Federal Reserve’s long-term target of 2 percent, but not overly alarming, if they’re only “transitory.” Looking at item subcategories, the notable price increases include energy (+23.8%), with the gasoline subcategory up 41.8%. Used cars and trucks were up 41.7%. I question if this is a data anomaly. It doesn’t feel correct, unless used commercial trucks are selling for a large premium. However, the CPI report did state, “the index for used cars and trucks rose 0.2 percent in July (month-to-month) after rising at least 7.3 percent in each of the last 3 months.” Finally, transportation services (mostly motor vehicle maintenance and repair) was up 6.4%.

The slowdown in motor vehicles parts and dealer sales in July, along with the 41.7% increase in used car and truck prices indicates that the supply constraints in automotive, partially caused by semiconductor shortages, is causing sales volume decreases and increased prices for alternatives such as used car purchases and automotive maintenance and repairs. The increase in energy prices is also important to monitor. Energy prices have played a role in much of the inflation within the recent past. If supply does not increase to offset excess demand, then high prices could persist and cause continued pricing pressure.

The July 2021 Manufacturing ISM Report On Business shows that economic activity in the manufacturing sector grew in July, with the overall economy notching a 14th consecutive month of growth. But the specifics highlight the breadth of supply constraints. The prices index went down from June. But the June price index reading since July 1979. An included quote attributed to T. Fiore, Chair of the ISM Manufacturing Business Survey Committee, was as follows, “Business Survey Committee panelists reported that their companies and suppliers continue to struggle to meet increasing demand levels. As we enter the third quarter, all segments of the manufacturing economy are impacted by near record-long raw-material lead times, continued shortages of critical basic materials, rising commodities prices and difficulties in transporting products.” The quote went on to name worker absenteeism, short-term shutdowns due to parts shortages, and difficulties in filling open positions as the issues limiting manufacturing growth potential. Fiore also noted transportation inefficiencies as an obstacle to increasing growth.

Final Word

These sources, and others, indicate acute supply constraints in certain areas, such as automotive, and other factors that appear to be more widespread, such as labor constraints. Other sources have attributed the labor shortage to increased unemployment benefits (soon to expire), frictional unemployment due to factors such as childcare requirements, and concerns with increased risk of COVID infection for certain high-risk jobs. Perhaps salary increases in jobs that are in high demand and now come with increased risk of infection, greater certainty surrounding the school year, and the expiring increased unemployment benefits, will direct activity that will reduce labor constraints and limit inflation to “transitory.”