COVID-19 caused a global upheaval in order fulfillment processes throughout 2020. As we enter the second half of 2021, there are abundant signs of improvement and optimization. Meanwhile, caution is prevalent as well. For example, the Delta variant of COVID-19 may cause an increase in infection and disruptions to business in the fall. Scenarios such as this, generally categorized as a surge, have been a concern for the last six-plus months. At the beginning of 2021, ARC Advisory Group, in partnership with DC Velocity magazine, anticipated factors such as a subsequent surge when we crafted our survey of warehouse practitioners. We obtained insights into experiences from the prior year (2020) and expectations for 2021 and beyond. Our research contained questions about numerous topics. However, this article will focus on findings about the following: business activity (anticipated change in order throughput volumes); COVID-19 related impacts on labor productivity; and perspectives on warehouse technology investments.

Warehouse Business Activity

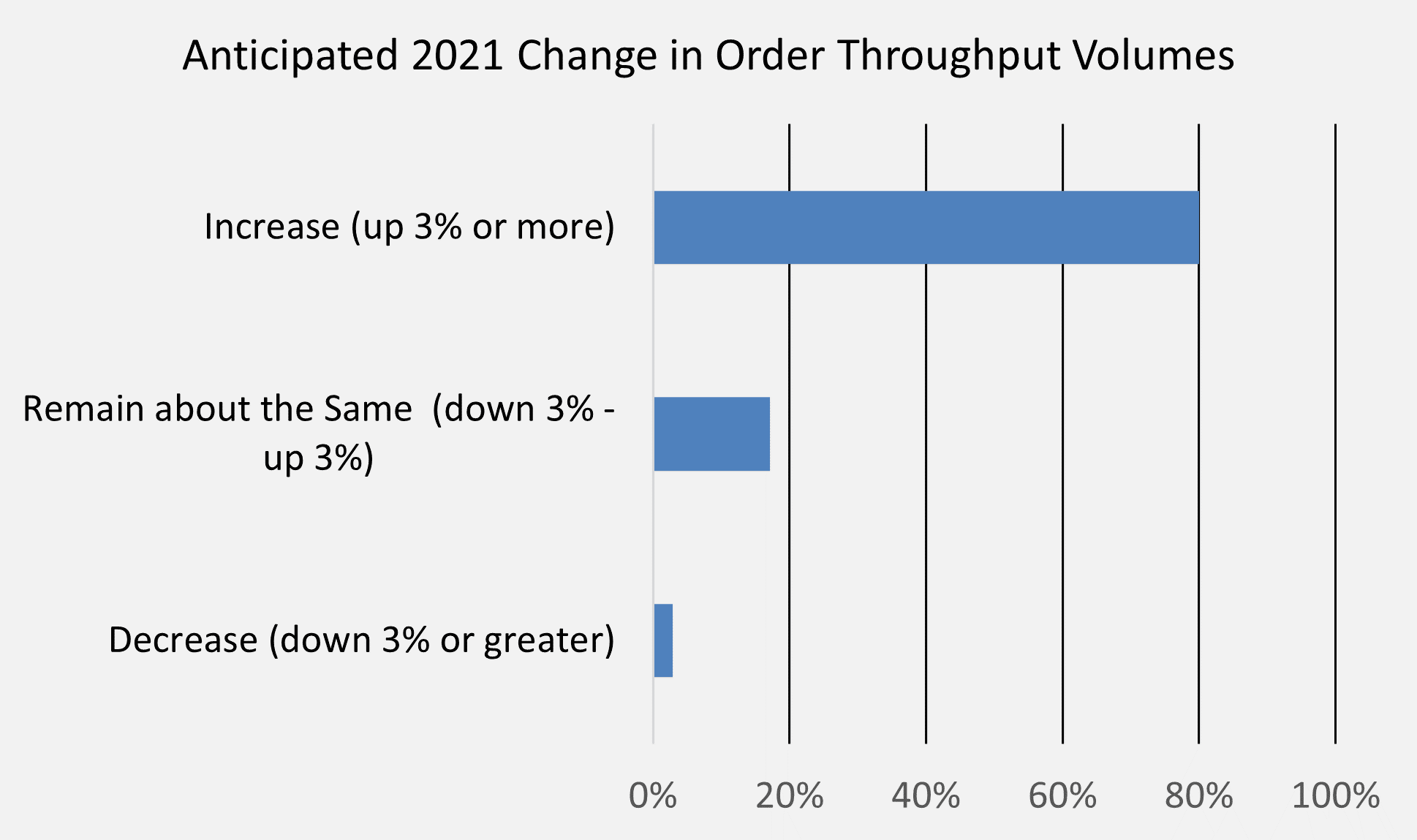

More than 25 percent of survey respondents stated that they experienced a decrease of order throughput volumes in 2020. In contrast, only 3 percent of respondents anticipate a decrease in 2021. Furthermore, 80 percent of respondents anticipate an increase of order throughput volumes, while only 17 percent expect volumes to remain about the same. These expectations are generally in-line with other broader economic measures of expectations such as the ISM Report on Business and other confidence measures. In general, our results indicate widespread optimism for 2021, accompanied by a health dose of caution.

COVID-19 Labor & Productivity Impacts

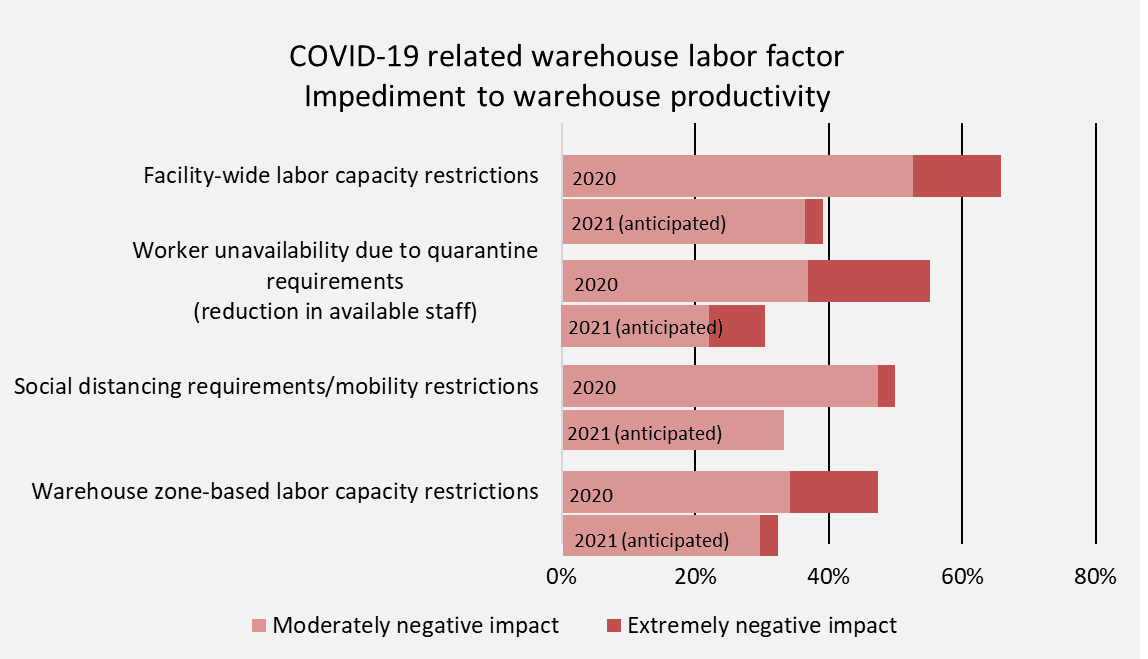

Labor productivity was hindered extensively by COVID-19 and these negative impacts were exerted through a number of mechanisms. Within warehouse and fulfillment operations, personnel and labor was negatively impacted in a few ways. In our survey, we inquired about the impacts of facility-wide labor capacity restrictions, warehouse zone-based labor capacity restrictions, social distancing requirements/mobility restrictions, and worker unavailability due to quarantine requirements (reduction in available staff). The first three mechanisms are driven by restrictions on personnel density or movement within a warehouse or facility. In contracst, the last mechanism (worker unavailability) is a temporary reduction in the size of the available labor pool. Aggregate responses indicate that facility-wide labor capacity restrictions was the factor that exerted the most widespread negative impact on 2020 warehouse operations. And although social distancing measures negatively impacted warehouse operations, one respondent stated that complying with social distancing measures was key to continuing operations. Most notably, negative impacts from worker unavailability due to quarantine requirements was almost as widespread as facility-wide labor capacity restrictions, but also exerted the greatest amount of “extremely negative impact” on warehouse operations in 2020. I view this result as “when quarantine requirements hit a warehouse operation, likely due to a local outbreak, they hit it hard.” When viewing the same factors for anticipated impediments to 2021 operations, a substantial improvement is visible across the board. Of course, expectations are uncertain. But the reduction in 2021 anticipated negative impacts, when compared to those that were experienced in 2020, indicates an improvement in expectations that to date have occured as expected (or better).

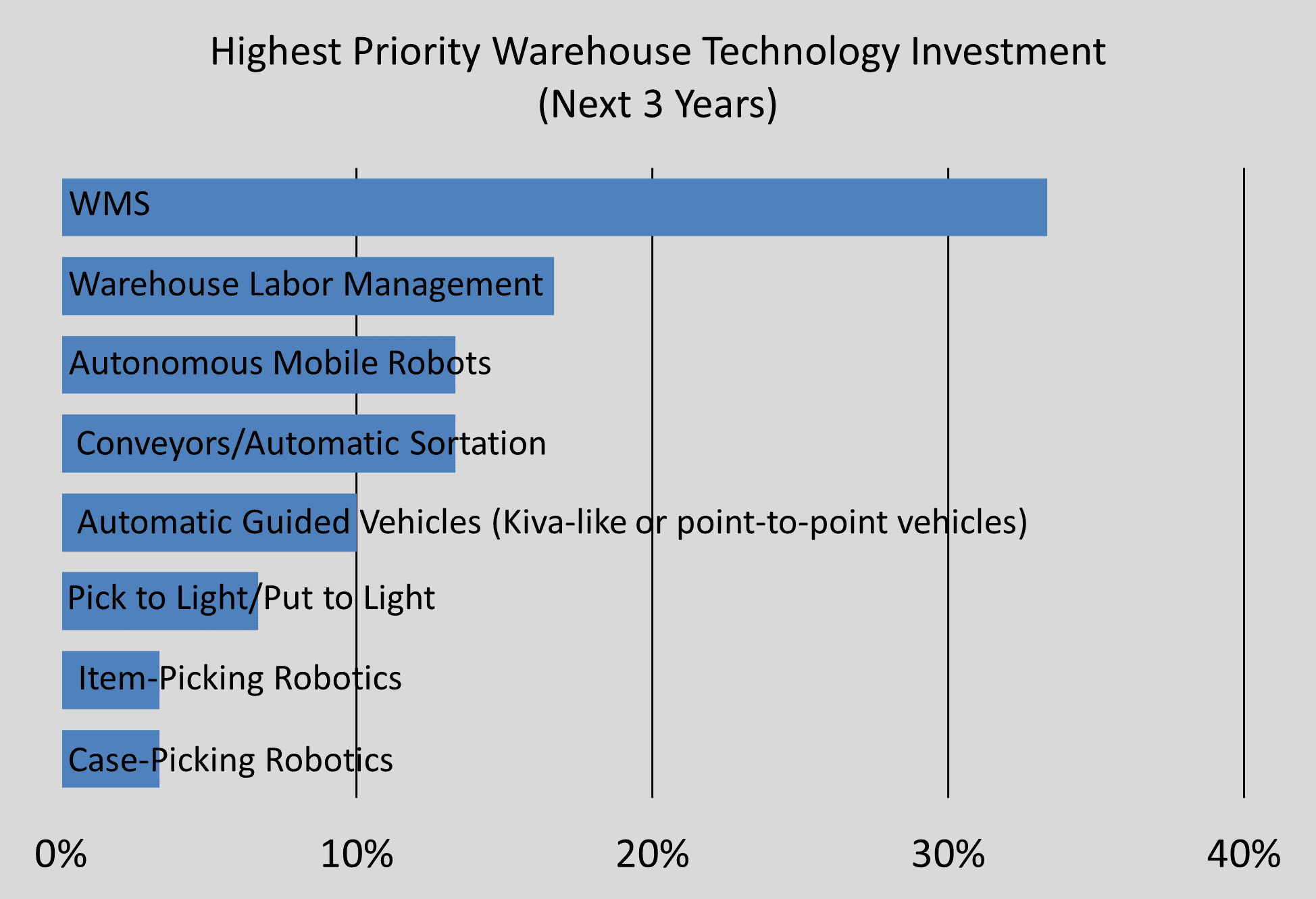

Warehouse Technology Investment Perspectives

ARC Advisory Group’s prior research with DC Velocity indicated that the value proposition of warehouse automation continues to improve. Our research this year indicates the same. Over 60 percent of respondents indicated that they believe the warehouse automation value proposition will expand (become more applicable) over the next three years. Meanwhile, less than 10 percent expect the value proposition to diminish (become less applicable). With that said, we asked respondents to identify the one warehouse technology investment that is the highest priority/importance to their organization. WMS was by far the most frequently chosen technology, followed by warehouse labor management. I believe these results indicate that software remains central to achieving efficient and effective warehouse operations, and that labor remains a necessity in the vast majority of facilities. With respect to automation, autonomous mobile robots (AMR) and conveyors/automatic sortation were most frequently chosen. Conveyors and sortation is almost a necessity to automated warehouses, so this was expected. However, the relatively high importance of AMRs shows that these robotic systems have matured rapidly from emerging to well-established warehouse technology options.