What is happening to global trade? You may ask, “What do you mean?” Well, I think a quote from a World Trade Organization (WTO) September press release describes the situation the best:

“If current projections are realised, 2015 will mark the fourth consecutive year in which annual trade growth has fallen below 3 per cent and the fourth year where trade has grown at roughly the same rate as world GDP, rather than twice as fast, as was the case in the 1990s and early 2000s.” (Emphasis mine)

Global trade has been growing at about twice the rate of global GDP for most of the last 20 years. This growth has been especially beneficial to the logistics industry and the technology vendors and others that support logistics operations. Given the importance of trade growth to the logistics industry, I decided to dig beneath the headlines to obtain a better understanding of the what, when, where, and how of this global trade slowdown.

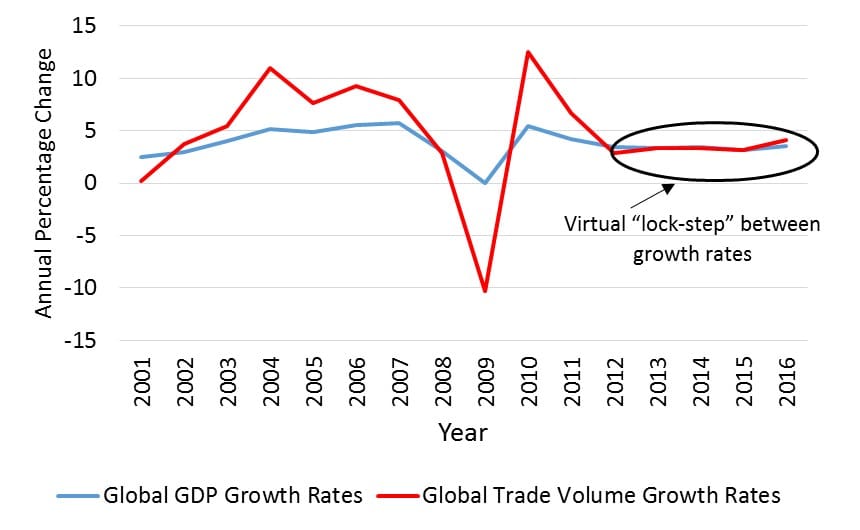

The adjacent image is a chart of data from the IMF. It provides visual perspective to the WTO quote above. Just from looking at this chart, it is apparent that global trade growth is more volatile global GDP growth. However, the second takeaway is that both data sets have been running in virtual lock-step since 2012, confirming the statement by the WTO. Global trade growth has settled to global GDP growth rates.

Digging Deeper Into the Specifics

Clearly global GDP growth, and global trade are about as all-inclusive as economic data can get. Is trade slowing across all regions, all cargo types, and all routes, or are there specific segments of the market that are dragging down the global aggregate data? The WTO publishes quarterly import and export trade volumes by region. The accompanying charts show quarterly export and import trends by region. North America and Europe look stable to strong over 2014 and 2015 Q1. In contrast, Asia and Other (CIS, Middle East, Africa) show a notable decline over that same period. At the same time, imports by South America and Other declined substantially. The WTO attributed the South America downturn to Brazil’s combination of fiscal difficulties and declining export prices (presumably reducing the country’s aggregate purchasing power).

The slowdowns in these shipping routes are pressuring freight rates across commodity classes. Drewry stated in its Dry Bulk Forecaster that China’s slowdown is negatively impacting iron ore and coal shipping demand. Meanwhile, the Wall-Street Journal reported that approximately 690 dry-bulk ships across the globe are currently sitting idle. However, this supply-demand mismatch is also a result of increased shipping capacity that has become available. Drewry also noted that there is a supply-demand imbalance in the container shipping segment, with the idle fleet near one million twenty-foot equivalents.

What about the US? Cass/Inttra published its ocean freight index through May 2015 (and halted publication thereafter). However, US container import activity looked stable in the first five months of 2015, but US exports were noticably weaker than the prior three years (see chart). It is difficult to determine if the slowdown in US exports is a result of slowing economies overseas, or if it is a result of the strengthening US dollar, leading to US exports being replaced by cheaper alternatives.

What about the US? Cass/Inttra published its ocean freight index through May 2015 (and halted publication thereafter). However, US container import activity looked stable in the first five months of 2015, but US exports were noticably weaker than the prior three years (see chart). It is difficult to determine if the slowdown in US exports is a result of slowing economies overseas, or if it is a result of the strengthening US dollar, leading to US exports being replaced by cheaper alternatives.

Conclusion

From a regional perspective, this data supports the view that diminishing demand in China, likely from reductions in infrastructure spending, is a root cause of the slowdown. Additionally, Brazil appears to be experiencing the strongest secondary effects from commodity price declines (reduced foreign capital from exports, leading to reduced capacity to import other goods). Also, I believe that the trade volume data provides support for the thesis that oil price declines are at least partially resulting from slowdowns in demand, as opposed to being exclusively a supply-side issue. In contrast, it is my opinion that other slowdowns in trade are residuals from the root causes listed above. Therefore, I believe pricing declines outside of bulk commodity transport will be more transitory and are more of a result of increased shipping capacity. Finally, let’s remember, all of this data is backward looking. So let’s hope this is only a temporary bump in the road that is now in our rearview mirror.

—

Omni-Channel Fulfillment Webinar

Interested in Omni-Channel Fulfillment? Register for a free webinar scheduled for March 10th, hosted by IBS and ARC Advisory Group, to hear about the findings from survey-based research on Omni-Channel Fulfillment. The webinar will be punctuated with contributions and insights by Graham Newland, IBS’ new Chief Customer Officer.

[…] What’s Happening to Global Trade? SupplyChainCircle.com is delighted to provide you with the above supply chain article. Please subscribe to our feed to get the latest in logistics and Logistics news. […]