How The Warehouse Automation Market is Evolving to Meet Practitioners’ Needs

The warehouse automation market has certainly evolved over the last two years. Thankfully, I believe most of the changes are advancements that allow suppliers to better meet customers’ needs. I will categorize the market’s evolution into three high-level categories – more holistic solutions, greater system adaptability, and greater system intelligence. Warehouse automation vendors have purchased other companies within the industry to expand their offerings, with recent examples including Dematic’s acquisition of SDI Group, obtaining its garment-on-hanger system, and Vanderlande’s acquisition of Dinamic, extending its portfolio of conveyors. The rapid growth of e-commerce; the heterogeneous nature of today’s items, orders, and loads; and the unpredictable business environment have made system adaptability and fulfillment flexibility increasingly important to fulfillment operations. Shuttle systems have been the ideal solution to meet these needs.

Yippee! I have officially completed ARC’s Warehouse Automation & Control Market Research Study. A short stint in editing is all that stands in the way of the study’s publication. Prior to the launch of this year’s study process, I reached out to industry participants and customers to find out how I could modify the study’s content to provide additional value. I took your feedback and included two additional sets of information. The first is a breakdown of hardware revenues across load sizes – Pallet, Tote/Carton, and Small Item. The second is a breakdown of total warehouse automation & control revenues to the retail industry, broken down by type of retailer – Apparel, Home Improvement, Pharma/Health & Beauty, Electronics, Department & General Merchandise, and Other Retail. ARC Advisory Service clients interested in purchasing the study should contact their account managers. Others interested in learning more about the study’s content and its availability for purchase can contact ARC here.

The warehouse automation market has certainly evolved over the last two years. Thankfully, I believe most of the changes are advancements that allow suppliers to better meet customers’ needs. I will categorize the market’s evolution into three high-level categories – more holistic solutions, greater system adaptability, and greater system intelligence.

More Holistic, Integrated Solutions

Warehouse automation and control systems (WAC) have been evolving into more holistic offerings for a number of years. This can be seen in the history of mergers and acquisitions within the industry- leading to larger suppliers offering a broader array of systems. Warehouse automation vendors have purchased other companies within the industry to expand their offerings, with recent  examples including Dematic’s acquisition of SDI Group, obtaining its garment-on-hanger system, and Vanderlande’s acquisition of Dinamic, extending its portfolio of conveyors. Of course, the recent acquisitions also extended outside of the traditional warehouse automation market to that of complementary businesses. The acquisitions of Dematic by KION (forklifts) and Swisslog by Kuka (robotics) are two of the most prominent. Clearly these companies engaged in acquisitions for business reasons. But these actions will also result in customers’ ability to purchase a greater range of solutions from a single provider. At the same time, warehouse automation suppliers are placing a premium on the capabilities of their warehouse control systems (WCS) and those systems’ ability to integrate and coordinate the various sub-systems across the warehouse. Swisslog’s acquisition of Forte Industries and Dematic’s acquisition of Reddwerks are both examples of large integrated suppliers acquiring smaller warehouse control system vendors to obtain their intellectual property, particularly their WCS and associated control system expertise. There are also warehouse automation suppliers such as Fortna, that offer a WCS that integrates and optimizes processes and third-party sub-systems across the warehouse. They do not develop their own material handling equipment, but instead serve as an intermediary between their client and the warehouse automation system providers. However, they still offer the risk reduction and accountability benefits of employing a general contractor. Of course, WAC suppliers aren’t only extending their offerings through acquisitions, they’re also expanding their offerings through in-house product development. In particular, shuttle systems have been an area of substantial investment for WAC providers. And shuttle system adaptability is a major selling point to these solutions.

examples including Dematic’s acquisition of SDI Group, obtaining its garment-on-hanger system, and Vanderlande’s acquisition of Dinamic, extending its portfolio of conveyors. Of course, the recent acquisitions also extended outside of the traditional warehouse automation market to that of complementary businesses. The acquisitions of Dematic by KION (forklifts) and Swisslog by Kuka (robotics) are two of the most prominent. Clearly these companies engaged in acquisitions for business reasons. But these actions will also result in customers’ ability to purchase a greater range of solutions from a single provider. At the same time, warehouse automation suppliers are placing a premium on the capabilities of their warehouse control systems (WCS) and those systems’ ability to integrate and coordinate the various sub-systems across the warehouse. Swisslog’s acquisition of Forte Industries and Dematic’s acquisition of Reddwerks are both examples of large integrated suppliers acquiring smaller warehouse control system vendors to obtain their intellectual property, particularly their WCS and associated control system expertise. There are also warehouse automation suppliers such as Fortna, that offer a WCS that integrates and optimizes processes and third-party sub-systems across the warehouse. They do not develop their own material handling equipment, but instead serve as an intermediary between their client and the warehouse automation system providers. However, they still offer the risk reduction and accountability benefits of employing a general contractor. Of course, WAC suppliers aren’t only extending their offerings through acquisitions, they’re also expanding their offerings through in-house product development. In particular, shuttle systems have been an area of substantial investment for WAC providers. And shuttle system adaptability is a major selling point to these solutions.

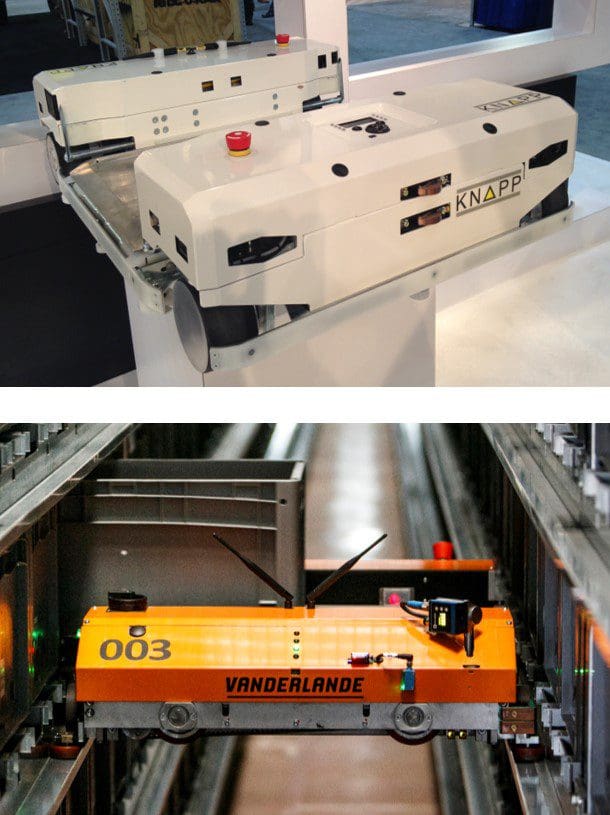

Greater System Adaptability

ARC, in partnership with DC Velocity, recently conducted an online survey of warehouse practitioners to obtain insights into fulfillment demands, investments, and shifting priorities. Our research results show “adaptability” (defined as the ability to handle a wide range of order profiles) as the fulfillment capability expected by most to increase in importance over the next five years. The rapid growth of e-commerce; the heterogeneous nature of today’s items, orders, and loads; and the unpredictable business environment have made system adaptability and fulfillment flexibility increasingly important to fulfillment operations. Shuttle systems have been the ideal solution to meet these needs. And numerous vendors are investing to improve upon the flexibility, speed, and reliability of their shuttle system offerings.

Shuttle systems have been in use for a number of years. However, there have been some recent advancements that have made these systems more adaptable. Of course, there are a number of means by which shuttle systems can increase in adaptability – namely the ability to interface with a wider range of load shapes and sizes, to coordinate and control the movement of the various shuttles, and to dynamically scale to meet volume requirements. But I will just mention a couple specific examples that I find interesting. The first is Knapp’s YLOG shuttle. In particular, I like the ability of the shuttles to move across levels and to make 90 degree turns (3D movement) in the racking system. These capabilities are made a reality by a flexible power system that allows freedom of movement and swiveling wheels that facilitate the 90 degree turns. The second is Vanderlande’s Adapto shuttle. The Adapto shuttle system is able to move across levels and make 90 degree turns (3D movement), similar to Knapp’s YLOG shuttle. However, Vanderlande’s shuttle utilizes a retractable set of wheels to facilitate the Z-axis movement.

Greater System Intelligence

More holistic and integrated solutions imply coordination of the parts and an increase in complexity. At the same time, more adaptable and dynamic systems also potential for increased levels of complexity. In fact, shuttle systems that allow dynamic movement require traffic control systems to coordinate the movement of the parts. At the same time, warehouse automation vendors are improving upon the intelligence of their warehouse control systems to control, coordinate, and optimize the movement of the disparate sub-systems within a warehouse. Suppliers are adding real-time optimization capabilities and more advanced reporting and analytical capabilities to support management decision-making. The value of these software capabilities is evident in the investment put into these systems such as Dematic iQ and then the company’s subsequent acquisition of Reddwerks; Swisslog’s acquisition of Forte Industries; and Intelligrated’s investment into its (formerly Knighted) software portfolio.

—

Coming soon to a Logistics Viewpoints blog post near you….the factors contributing to growth of the global warehouse automation & control market.

AI Is Reshaping Supply Chain Execution. Here’s What Comes Next.

Two ARC Advisory Group white papers on the next stage of AI in supply chain operations.

AI is moving beyond isolated copilots and technical architecture into coordinated operational decision systems. This ARC Advisory Group white paper explains how supply chain AI is shifting from capability to execution, where context, governance, workflows, thresholds, and action pathways determine whether AI improves real decisions across planning, logistics, sourcing, fulfillment, and risk management.

Download Our Featured White Paper:

AI in the Supply Chain Part II: From Architecture to Execution - Defining the Decision Intelligence Layer in Modern Supply Chain

Download Our Foundational White Paper:

AI in the Supply Chain: Architecting the Future of Logistics with A2A, MCP, and Graph-Enhanced Reasoning

Explore Our Domains

Planning, Execution & Visibility | Transportation & Logistics Operations | Warehousing, Fulfillment & Automation | Global Trade & Compliance | AI & Advanced Analytics | Data, Integration & Interoperability | Supply Chain Platforms | Risk & Resilience | Sustainability & ESG

Independent ARC research for supply chain leaders and technology decision-makers.