Forwarders and brokers are a critical part of international supply chains. They operate in incredibly competitive markets that can be characterized by tight margins and highly influenced by regulatory change. This past spring, we conducted a benchmark study with over 100 forwarders and brokers to evaluate how macroeconomic changes were impacting them, the strategies and tactics they were using to be successful and the importance of technology to their business. Below, we’ve included some of the findings of the benchmark study. Regardless of whether you are a forwarder or broker, you are going to want to read this post for the lessons learned here that apply to all industries.

Tough market to make money

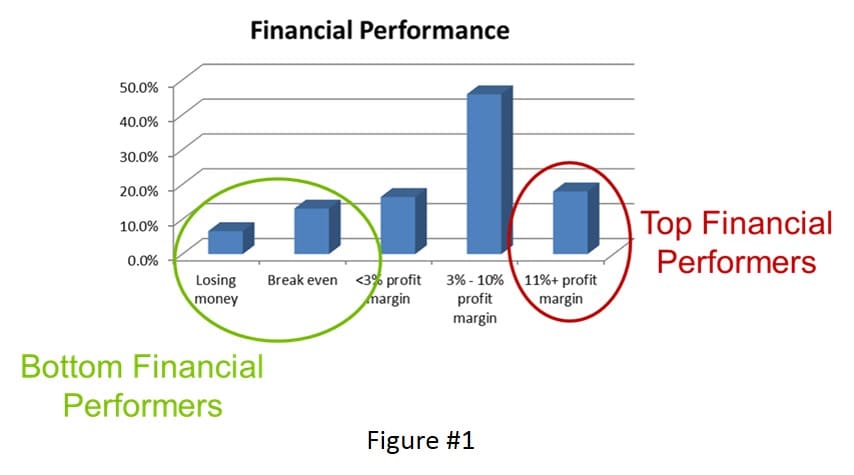

We asked forwarders and brokers about their profit margins and, as you can see in Figure #1, those margins are pretty thin. Profit margins have been under severe pressure for a number of years as importers and exporters have been very cost focused and many forwarders and brokers have struggled to differentiate themselves. Almost 20% of the survey participants are challenged to be profitable at all and slightly less than 20% have strong financial performance.

There’s a wide gap between the “haves” and “have nots”. So, we took a look at the data from the perspective of the bottom and top financial performers, – and this is what we found.

Global instability and regulatory change are top of mind

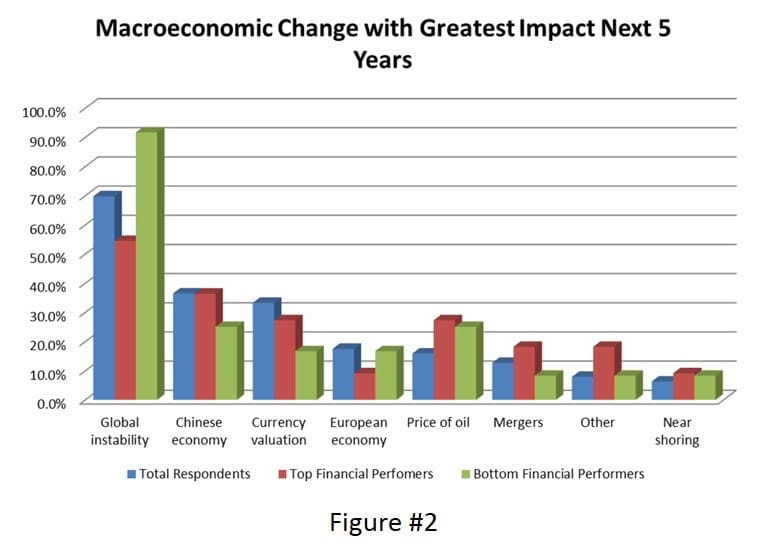

By a 2:1 margin for all respondents, global instability was reported as the top macroeconomic driver. Over 90% of the bottom financial performers stated it was their major concern as opposed to 50% of the top financial performers (see Figure #2). The bottom financial performers tended to be the smaller forwarders and brokers and, as we will illustrate later, they’re not necessarily focused on the key elements for stability or financial success.

Regulatory changes also dominated forwarder and broker agendas. With over 80% of the respondents citing that they had US operations, it was no surprise that the US Advanced Commercial Environment (ACE) change underway was the top concern. It is interesting to note that 67% of the bottom financial performers as opposed to 45% of the top financial performers thought ACE was the top regulatory issue (see Figure #3). Based upon experience with thousands of forwarder and broker customers, we believe that this is because the bottom financial performers wait until the last moment to become compliant, as opposed to the top performers who tend to have more resources and invest early to achieve compliance to changing regulations.

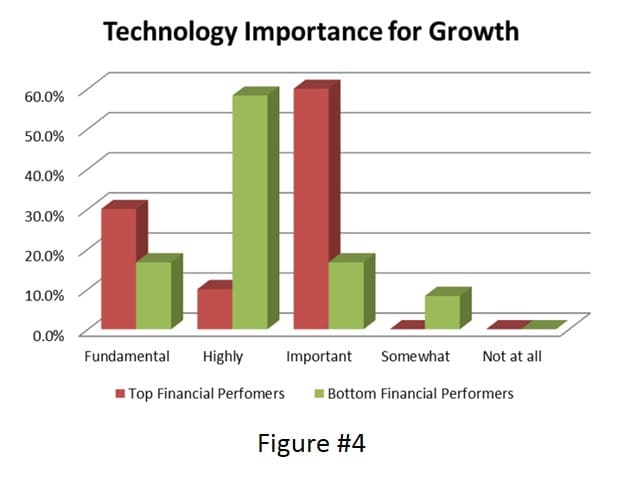

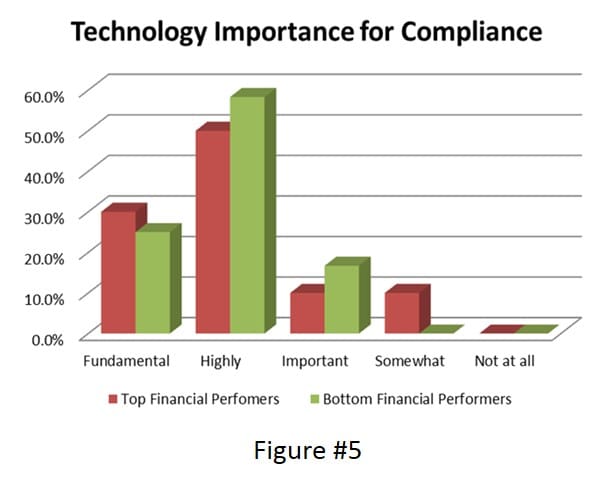

IT is critical, but viewed as infrastructure to support initiatives

Technology, especially related to regulatory compliance, was also top of mind for all respondents. However, given the responses on industry change (see Figures #4 & #5), over 75% of respondents said that they were going to spend more on IT in the next 2 years than they had previously. “High service level” (71%) was cited as the top competitive weapons and it was even more important for top financial performers (82%). We believe that the bottom financial performers are more heavily investing to gain or maintain compliance and catch up with customer demands for advanced capabilities like purchase order management and shipment visibility.

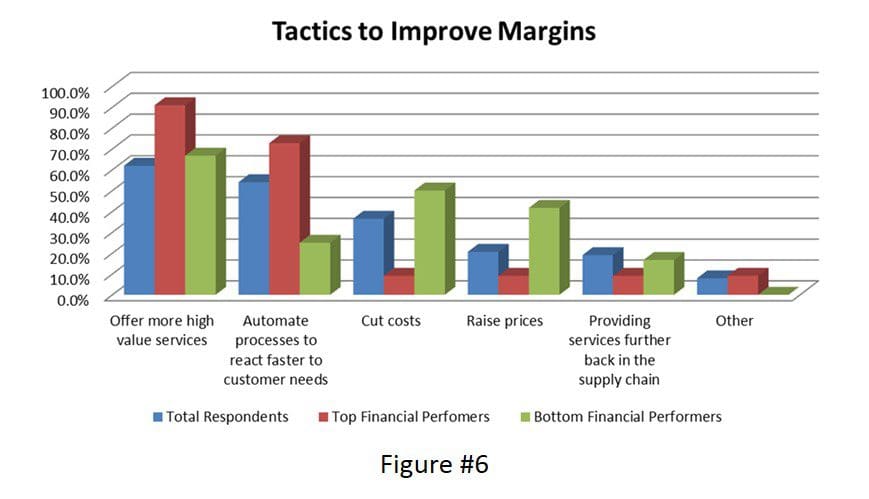

Strategies and tactics differed significantly by financial performance. From a financial performance perspective, the strategies and tactics directly aligned with financial performance. Top performers are more prepared for change and growth by being customer focused (36% versus 8%). In addition, top financial performers are more focused on the services that improve margins. Bottom financial performers were more focused on financial mechanics like cost cutting and raising prices to improve margins.

Regardless of whether you are a forwarder and broker, this benchmark study has some valuable lessons for every organization. Financial performance is a function of your company’s strategies and tactics that drive value for your customers. It’s not driven by financial “engineering”. In addition, investing proactively allows the organization to be in better control of its destiny and not just reactive to industry change. To learn more, go to Forwarder Broker Benchmark Survey to get the study ebook.

As Executive Vice President, Marketing and Services, Chris Jones is primarily responsible for Descartes marketing activities and implementation of Descartes’ solutions. Chris has over 30 years of experience in the supply chain market, including the last 10 years as a part of the Descartes leadership team. Prior to Descartes, he has held a variety of senior management positions in other organizations including: Senior Vice President at The Aberdeen Group’s Value Chain Research division, Executive Vice President of Marketing and Corporate Development for SynQuest and Vice President and Research Director for Enterprise Resource Planning Solutions at The Gartner Group and Associate Director Operations & Technology for Kraft Foods.