One year ago, there was debate about whether the recently inverted US treasury yield curve was a sign of a forthcoming recession. We took a moment to evaluate the current environment last December. Recent data indicated soft manufacturing activity coinciding with ongoing trade disputes. These data points provided credibility to the view that a recession was possible. In hindsight, fourth quarter 2019 US GDP did decline slightly. But that decline was greatly overshadowed by the subsequent impact of Covid-19 on economies across the globe. I find it interesting to look back and see how much things have changed in one year. So where are we today? Let’s look at some of the same economic indicators as we did last December, and some additional ones.

World Trade Organization – International Trade

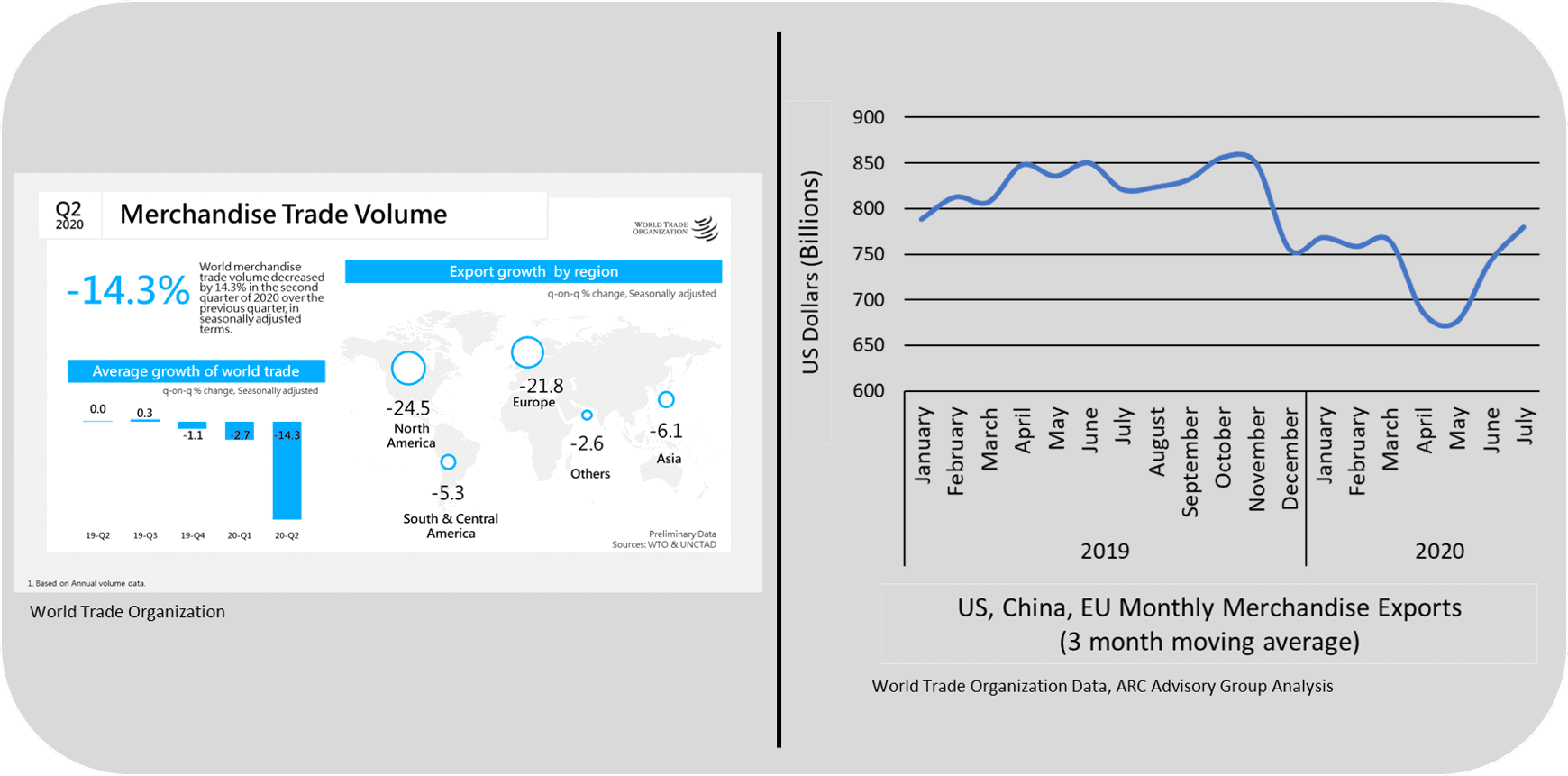

The World Trade Organization publishes monthly merchandise trade data. In an effort to obtain a pulse on global trade, I reviewed the export data of the US, European Union, and China. China export data was unavailable for January 2020. I am unsure at this time if that is erroneous data or a reflection of China’s January lockdown. Regardless, that data point skews the trend. I aggregated the export data from these three large economies and developed a three-month moving average. The trend line shows that export trade activity declined by about 20 percent from the pre-Covid trend and subsequently regained half of that deficit in the summer months. This data shows that trade is on a sustained growth trend but still remains below pre-Covid levels.

US Government Statistics

US government data provide more recent insights into US exports and overall GDP. The US Census Bureau’s Advance Economic Indicators Report for October shows that exports were up 8.9 percent from the prior month (September), but down 7.1 percent from October 2019 (year over year). This confirms a continuation of the growth trend with overall activity levels still below the pre-Covid trend.

US Real gross domestic product (GDP) increased at an annual rate of 33.1 percent in the third quarter of 2020. But, similar to my comments in August about the headline GDP contraction of 33 percent for Q2; these are annual rates – or the total change that would occur if the current rate of change continued sequentially for a whole year. I find these annualized rates to be more useful in stable times than they are in the more volatile periods of the last year. In this environment I find actual period-to-period changes to be more informative. The actual GDP dollar estimate for Q3 2020 is up 7.4 percent from Q2 2020. Meanwhile, gross private domestic investment in equipment (relevant for transportation equipment and warehouse automation equipment) is up 13.5 percent over that same period – with general industrial, including material handling equipment, up 9.0 percent. These macroeconomic data points also suggest that the economic context remains on a growth path. However, private investment in non-residential structures continued to decline in Q3. This decline appears to be a result of weakness in office and retail, rather than industrial and warehousing properties. CBRE stated in its 2021 Real Estate Market Outlook that the US Industrial and Logistics property category will “continue to flourish” in 2021. Further stating that demand will be driven by an increase in online sales.

ISM Report on Business

Purchasing managers indexes are often considered leading indicators of overall economic activity. The ISM released its November Manufacturing Report on Business yesterday morning. The November PMI registered 57.5 percent, indicating an expansion of the manufacturing sector. The report implied that the sector is growing a slower rate than the previous month, with input-driven constraints being the main inhibitor to growth. Meanwhile, the October Services Report on Business also indicated ongoing growth, with Transportation & Warehousing listed prominently as an industry reporting growth in business activity, new orders, and employment. But the ISM Reports on Business provide a directional trend and some idea of magnitude but do not provide insight into the overall level of activity. And given the abrupt and deep downturn of Q2 2020, growth at this point certainly does not imply an economy running at full capacity.

Final Word

The wealth of public data available for analysis points to a clear overarching trend. The US economy and global trade continue to grow off the deep contraction caused by the Covid-19 lockdowns earlier in the year. However, economic activity still remains below the pre-Covid-19 levels. Input constraints, such as social distancing and quarantines, continue to serve as a primary inhibitor of growth. Meanwhile, the logistics industry continues to experience above average growth due to the ongoing transition and likely acceleration to e-commerce and direct-to-consumer fulfillment.

{kind=link}