By definition, omni-channel is a term that describes an intersection, or an interplay between commercial “pathways”, and it is also a term that describes a cross-section of business processes. There is the sales aspect of omni-channel as well as the fulfillment and customer service aspects. My colleague Chris Cunnane and I, in partnership with James Cooke of DC Velocity, are in the final stages of a comprehensive research project on omni-channel fulfillment. We surveyed numerous pure-play retailers as well as brand manufacturers that sell directly and indirectly through retail partners. And we obtained feedback on a number of dimensions related to omni-channel fulfillment, including:

- Sales channels, to obtain an understanding of the principal go to market profiles

- Fulfillment resources deployed (corporate DCs, 3PL managed fulfillment, retail locations)

- Business processes and technology utilized

- The interplay or integration of these dimensions and categories (essentially what distinguishes “omni-channel” from “multi-channel”)

- A time element: the current state, the past state, and the anticipated change in important aspects to the topic

We are just beginning to analyze the survey response data at this point. Chris, James, and I will be presenting our findings at CSCMP next month. There will also be a research summary published in DC Velocity this November. However, I reviewed the data briefly and I have already found some interesting insights. Some of the findings confirmed my existing perceptions, while others challenged them.

- I found it a bit surprising that the use of paper-based WMS was still 70 percent as prevalent as the use of radio-frequency (real-time) WMS solutions in traditional DCs (of companies that sell through retail partners). Real-time WMS was shown to provide a compelling ROI years ago. I’m interested in obtaining a better understanding of the resistance to WMS upgrades in these finished goods warehouses.

- For In-store fulfillment of e-commerce orders, more respondents indicated that order picking was done in the front of the store (store floor) than in the back rooms. I found this to be intuitive from a space utilization perspective, but less than ideal from an inventory accuracy or process efficiency perspective. Also, RF-based picking of e-commerce orders at the store was wide-spread, but still the exception rather than the rule.

- The use of distributed order management (DOM) solutions is almost as prevalent as that of WMS by the response base. I presumed that DOM was widely implemented due to its critical role in omni-channel operations, but not to that degree. My colleague Chris Cunnane will be conducting a quantitative study on the omni-channel technology footprint later this year that will include an assessment of the annual revenues from global DOM sales.

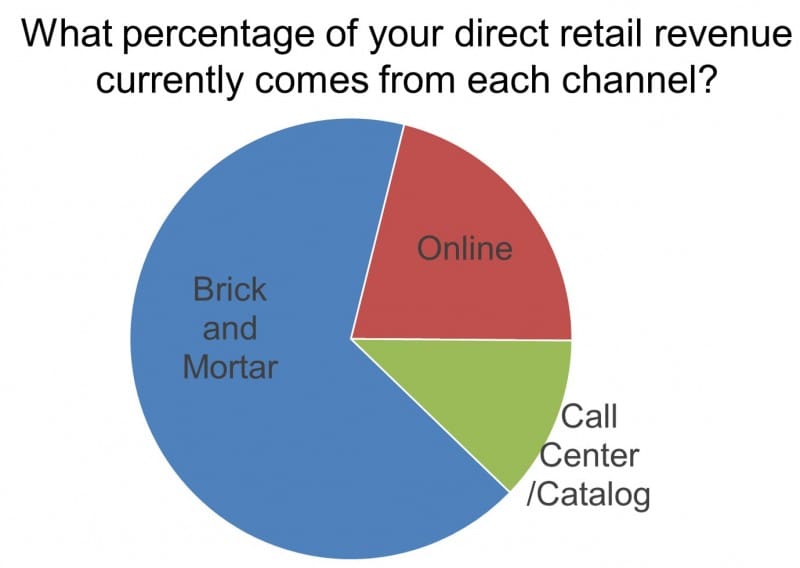

- Finally, as a benchmark of revenue generation by channel, on average, brick and mortar represented 70% of the respondents’ current revenue. But unsurprisingly, respondents expect that online revenue will increase more than brick and mortar revenue over the next five years.

If you are attending CSCMP next month, we will be presenting our results on Monday morning in the Omni-Channel track. If not, please keep an eye out for the summary article in DC Velocity this November.

Leave a Reply