Last week I read the Logistics Viewpoints guest post by Chainalytics discussing the pitfalls of decision-marking biases. Although the Chainalytics article focuses on supply chain decision making, these biases can apply to business forecasting as well. Reading this article made me interested in my own potential decision-making biases. I chose to take time on Friday to review some of the research I have conducted during my ten years as an analyst at ARC Advisory Group. Hopefully this review would provide me with insight into my past forecasting performance and the accuracy of my predictions. Ultimately, I believe that greater self-awareness will improve my feel for the dynamics of the supply chain technology markets and also improve my future forecasts.

Logistics Viewpoints articles typically discuss topics that are current and top of mind, as they should. But an occasional examination of the past can deliver interesting insights, so I decided to discuss my historical analyses of the the supply chain planning (SCP) software market and the warehouse management systems (WMS) market in this blog post.

WMS Market 2010 to Today

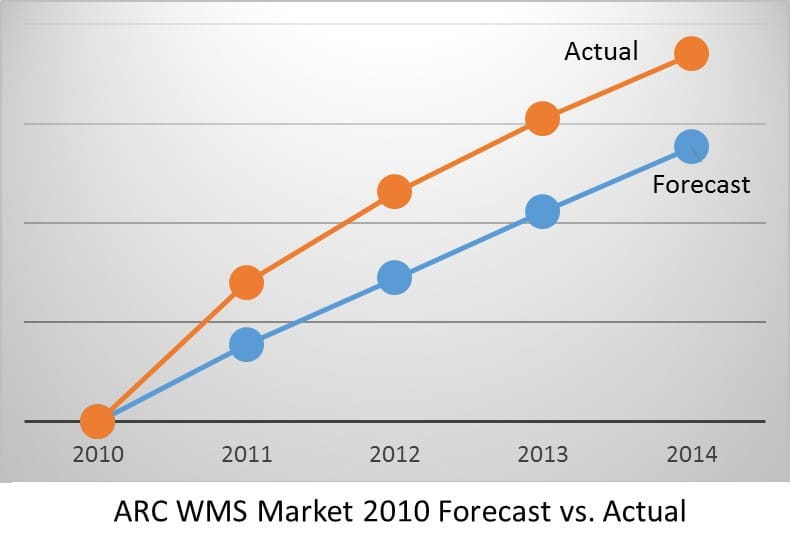

The year 2011 was the first time I conducted analysis on the global WMS market. I did this with Steve Banker, who had been researching the WMS market for almost 15 years by that time. The recent global economic downturn made forecasting of software sales particularly difficult at this time. The WMS market had for the first time contracted substantially in the previous year (2009). It returned to growth in 2010, but the growth was negligible compared to the previous year’s contraction (in essence, the downturn erased the four previous years of growth).

For the 2011 -2015 WMS forecast, Steve and I gathered and analyzed a wide range of data including vendors’ aggregate views on growth potential, past WMS and other SCM technology market growth rates, and past relationships between GDP growth and technology spending. We concluded that the WMS market would experience above average growth in the near future and then gradually revert back toward the long-term historical growth rate. Unfortunately (but fortunately for WMS software vendors) we underestimated the pent-up demand that built during the recession and therefore underestimated the spending bounce that would occur in 2011. It turns out that the WMS market grew by about 14 percent that year, almost twice as much as we had forecast. This underestimation had lasting effects on the difference between our forecast market size through 2015 and our future base-year estimates of the market’s size for each of the following years (ARC updates the global WMS study annually. Our forecast growth rates were largely in-line with actual growth going forward). In addition, I also underestimated the increased demand for WMS solutions that would be driven by the rapid and ongoing increase in e-commerce fulfillment. I expected e-commerce growth, but the degree to which it stimulated WMS sales far surpassed my expectations.

For the 2011 -2015 WMS forecast, Steve and I gathered and analyzed a wide range of data including vendors’ aggregate views on growth potential, past WMS and other SCM technology market growth rates, and past relationships between GDP growth and technology spending. We concluded that the WMS market would experience above average growth in the near future and then gradually revert back toward the long-term historical growth rate. Unfortunately (but fortunately for WMS software vendors) we underestimated the pent-up demand that built during the recession and therefore underestimated the spending bounce that would occur in 2011. It turns out that the WMS market grew by about 14 percent that year, almost twice as much as we had forecast. This underestimation had lasting effects on the difference between our forecast market size through 2015 and our future base-year estimates of the market’s size for each of the following years (ARC updates the global WMS study annually. Our forecast growth rates were largely in-line with actual growth going forward). In addition, I also underestimated the increased demand for WMS solutions that would be driven by the rapid and ongoing increase in e-commerce fulfillment. I expected e-commerce growth, but the degree to which it stimulated WMS sales far surpassed my expectations.

SCP Market 2006 to Today

I mentioned in an LV post last September that the 2005 supply chain planning (SCP) study was the first market study I developed as an ARC analyst. Needless to say, the SCP market has experienced substantial changes over the last ten years. In 2006 multi-echelon inventory optimization (MEIO) start-ups were “the next big thing” and the ERP vs. Best-of-breed debate was raging strong. As JDA noted in a recent LV guest post, the best-of-breed vs. ERP argument is largely history because today’s marketplace is much more dynamic and complex than it was in the past. Not to mention that best-of-breed suppliers have developed platforms that provide the integration and visibility benefits of an ERP system, and ERP vendors have improved the features and functionality of their supply chain solutions to better compete with best of breed vendors. And to bring it all together, today’s best-of-breed SCP and ERP vendors have acquired most of those MEIO vendors to augment their SCP solution footprints with more advanced optimization capabilities.

I mentioned in an LV post last September that the 2005 supply chain planning (SCP) study was the first market study I developed as an ARC analyst. Needless to say, the SCP market has experienced substantial changes over the last ten years. In 2006 multi-echelon inventory optimization (MEIO) start-ups were “the next big thing” and the ERP vs. Best-of-breed debate was raging strong. As JDA noted in a recent LV guest post, the best-of-breed vs. ERP argument is largely history because today’s marketplace is much more dynamic and complex than it was in the past. Not to mention that best-of-breed suppliers have developed platforms that provide the integration and visibility benefits of an ERP system, and ERP vendors have improved the features and functionality of their supply chain solutions to better compete with best of breed vendors. And to bring it all together, today’s best-of-breed SCP and ERP vendors have acquired most of those MEIO vendors to augment their SCP solution footprints with more advanced optimization capabilities.

My forecast growth rate for the SCP market fell short of the actual growth rate, similar to my forecast for the WMS market. However, the factors behind the forecast to actual variance differed greatly. In 2006, it appeared that ERP vendors would successfully displace much of the best of breed market share through pricing pressures and integration benefits. Although some ERP vendors did make substantial market share gains, the results were more subtle than I initially expected. In addition, S&OP processes continued to grow in popularity and those processes relied heavily on SCP applications. Finally, the improvement in computing power allowed for real-time supply chain scenario analysis and the ability to analyze data at a more granular level, thereby expanding the value proposition and ROI of many SCP solutions.

Lessons Learned

I am a firm believer in the golden rule of forecasting, to be conservative. However, the review of my past WMS and SCP market forecasts shows that even the golden rule of forecasting can be over weighted. In the case of the WMS and SCP market, I believe that I also over weighted the recent developments and trends in the market and under estimated the ability for markets to enter new growth phases driven by unforeseen factors. I believe my prior market forecasts were approximately correct but also realize that my new found awareness of underestimating future growth has helped me recognize my own decision-making biases and will hopefully contribute to improvements in my future logistics market forecasts.