Note: Today’s post is part of our “Editor’s Choice” series where we highlight recent posts published by our sponsors that provide supply chain insights and advice. This article is from Manhattan Associates and looks at the changing nature of retail.

Note: Today’s post is part of our “Editor’s Choice” series where we highlight recent posts published by our sponsors that provide supply chain insights and advice. This article is from Manhattan Associates and looks at the changing nature of retail.

Making predictions about the future of retail – or anything – can be a fool’s errand. However, retail as a whole has experienced a period where the future is being thrust upon it at an alarming rate. As that has occurred, plenty of leading indicators have emerged to shed light on what’s essential now, and what may be around the corner.

One place to look is stores. The pandemic forced retailers to push their limits. Contactless payment methods like pay-by-link exploded. The sudden demand for store fulfillment of online orders has added costs for handling and shipping, causing delays in delivery when carriers were stretched beyond their limits. Omnichannel systems, or lack thereof, were tested daily. And during the height of the pandemic, much of this happened without a single walk-in shopper at the store.

Later, the same demand was compounded by the sudden wave of curbside pickups. Then as stores started to reopen, buy online, pickup in-store (BOPIS) orders exploded as well. Stores quickly became hubs for returns of online purchases.

All told, changes that might have occurred over the course of a few years, have happened in months. Consumer expectations for service and speed rose just as quickly, and there is no reason to think they will not continue to gather steam in the near future.

In terms of interactions between brands and their customers, the status quo has been permanently transformed. In fact, 97 percent of retailers expect BOPIS and Curbside Pickup to stay the same or increase.

How is Retail Changing

Even prior to 2020, the stores had begun to serve multiple purposes. They were no longer a distinct, isolated channel, but rather, part of the overall brand experience. For some consumers, stores might be the start of a buying journey. For others, they may be a place to pick up orders or make returns. Today, stores are an integral part of the omnichannel experience, playing a different role for each person.

Despite many recent changes, one thing has remained clear: people have not stopped going into the store. While consumers are shopping online more than ever, 48 percent of US adults report that they purchase products or services in-store at least weekly — and 51 percent say they do so more often than that. That’s because stores offer extraordinary convenience due to proximity, knowledgeable staff and new, frictionless services.

Will Retail Survive as We Know It?

It is a certainty that retail will survive. It is almost as certain that retail, as consumers have known for decades, is permanently changed. The rise of omnichannel, the surge in online shopping and the explosion of new fulfillment options, have forced retailers to adapt quickly. For those with legacy technology, operational adjustments are happening despite their solutions rather than because of them. That’s because those solutions were designed for retail as it was, not for where retail is going.

Therefore, brands are rethinking the best ways to serve customers who have become accustomed to new, omnichannel conveniences. There is a critical interplay between online experiences and store experiences. But the technology of yesteryear is unable to bridge those two channels. While store teams have performed admirably, scrambling to meet new demands, reliance on outdated technology means experience and profitability have taken hits. The only way to sustain profitability and deliver the experiences customers increasingly demand is with a modern unified omnichannel platform, where point of sale, order management, customer engagement and fulfillment are linked and working in concert.

Here are some interesting stats:

- An increase in the volume of online orders fulfilled from stores has led to reduced profitability for 79 percent of retailers

- 72 percent of retailers are planning to increase store space dedicated to online order fulfillment

- 91 percent of shoppers miss shopping in stores, and “getting out of the house” is one of the top three motivators for future store visits

- 100 percent of shoppers miss the instant gratification of store purchases.

Will Retail Stores Exist in the Future?

The days of stores being a single, isolated selling channel are over. The physical store must now serve a range of purposes. New omnichannel services are likely permanent fixtures in retail, as shoppers enjoy being able to buy and return items wherever, whenever and however it’s easiest for them. To maintain customer loyalty, offering those conveniences will need to be continued. And to maintain margins, true omnichannel solutions are now critical. Success depends upon embracing new realities with machine learning technology that provides customer insights and services that facilitate seamless, flawless experiences at every point of interaction.

To read the full article, click HERE.

Sunday night brought a lunar eclipse. But this wasn’t any ordinary lunar eclipse. This was a total lunar eclipse of a super moon (a super full moon). A rising super full moon looks much larger than a normal full moon as it is closer to the Earth. Total eclipses of super full moons are not exactly common. In fact, the last one occurred in 1982 and the next will not occur until October 8, 2033. The eclipse left the super moon glowing red in the sky, with most people referring to it as a blood moon. It was a spectacular site to see, and I was fortunate enough to enjoy it while sitting around a fire pit with friends. It was a nice way to close out last weekend – along with watching Tom Brady join the 400 touchdown club.

Sunday night brought a lunar eclipse. But this wasn’t any ordinary lunar eclipse. This was a total lunar eclipse of a super moon (a super full moon). A rising super full moon looks much larger than a normal full moon as it is closer to the Earth. Total eclipses of super full moons are not exactly common. In fact, the last one occurred in 1982 and the next will not occur until October 8, 2033. The eclipse left the super moon glowing red in the sky, with most people referring to it as a blood moon. It was a spectacular site to see, and I was fortunate enough to enjoy it while sitting around a fire pit with friends. It was a nice way to close out last weekend – along with watching Tom Brady join the 400 touchdown club. Many large retailers are still working through inventories built up during the first half of the year. This is due to the swelling inventories that resulted from the clearing of backlogs at West Coast ports due to labor disputes. As a result, economists say that a shipping slowdown should occur before the holidays. Many retailers are seeing inventory levels at least 10% higher than this time last year. This is causing margins and profitability to take a hit. Due to these factors, the latest Global Port Tracker report by the National Retail Federation and Hackett Associates LLC projects only modest growth in container imports at U.S. gateways this fall.

Many large retailers are still working through inventories built up during the first half of the year. This is due to the swelling inventories that resulted from the clearing of backlogs at West Coast ports due to labor disputes. As a result, economists say that a shipping slowdown should occur before the holidays. Many retailers are seeing inventory levels at least 10% higher than this time last year. This is causing margins and profitability to take a hit. Due to these factors, the latest Global Port Tracker report by the National Retail Federation and Hackett Associates LLC projects only modest growth in container imports at U.S. gateways this fall. FedEx has a headache. The reason? A huge increase in the number of large, bulky shipments that customers expect delivered to their doors. An increase in online shopping has resulted in an increase in large goods that need to be shipped. These were items that were usually left to the customer to figure out how to get them home. This poses problems for a company that was built to move small packages. But now, large items, including everything from trampolines and mattresses to furniture and appliances, are being shipped through FedEx. FedEx allows companies to ship anywhere in the world at a rate that is more affordable than freight. But consumers are about to pay more for the privilege of getting large online purchases sent home. FedEx’s surcharge for parcels it considers over-sized will rise 17 percent to $67.50 on Jan. 4. UPS’s rate is $57.50, the same as FedEx’s current fee. FedEx also is increasing its base package shipping rates by an average 4.9 percent.

FedEx has a headache. The reason? A huge increase in the number of large, bulky shipments that customers expect delivered to their doors. An increase in online shopping has resulted in an increase in large goods that need to be shipped. These were items that were usually left to the customer to figure out how to get them home. This poses problems for a company that was built to move small packages. But now, large items, including everything from trampolines and mattresses to furniture and appliances, are being shipped through FedEx. FedEx allows companies to ship anywhere in the world at a rate that is more affordable than freight. But consumers are about to pay more for the privilege of getting large online purchases sent home. FedEx’s surcharge for parcels it considers over-sized will rise 17 percent to $67.50 on Jan. 4. UPS’s rate is $57.50, the same as FedEx’s current fee. FedEx also is increasing its base package shipping rates by an average 4.9 percent. Chipotle says carnitas is back on the menu at 90 percent of its restaurants, and that the pork’s return to all U.S. restaurants should be complete by the end of November. The restaurant chain had stopped serving pork at nearly one third of its restaurants after one of its suppliers violated its animal welfare standards. The company says it does not allow its pork suppliers to use gestation crates or antibiotics, and that pigs have to be given access to the outdoors. That makes it difficult to secure enough pork and puts major stress on its supply chain. However, this stance on animal welfare standards is also one of the restaurants biggest differentiating factors in a crowded market.

Chipotle says carnitas is back on the menu at 90 percent of its restaurants, and that the pork’s return to all U.S. restaurants should be complete by the end of November. The restaurant chain had stopped serving pork at nearly one third of its restaurants after one of its suppliers violated its animal welfare standards. The company says it does not allow its pork suppliers to use gestation crates or antibiotics, and that pigs have to be given access to the outdoors. That makes it difficult to secure enough pork and puts major stress on its supply chain. However, this stance on animal welfare standards is also one of the restaurants biggest differentiating factors in a crowded market. Clearpath Robotics announced its first self-driving warehouse robot: OTTO. This self-driving robot is capable of hauling one metric ton and a half of payload. That’s about 3300 pounds to you and I. Self-driving robots are nothing new to warehouses. In fact, we’ve written about Amazon’s robots, acquired from Kiva Systems, many times before. The difference is that unlike Amazon, these robots do not require navigation devices (RFID, barcodes, etc.). Instead, they have 20-meter lasers front and back (with an option for 50-meter range), and can localize against an existing basemap with an accuracy of about an inch (according to Clearpath). The new robots are in the midst of five pilot programs, the first being a General Electric facility (GE Ventures is a strategic investor in the project). It will be interesting to see how these robots perform in the field, and what impact they may have on the future of autonomous warehouses.

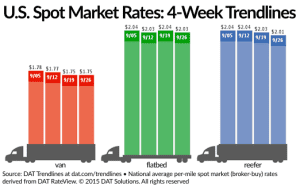

Clearpath Robotics announced its first self-driving warehouse robot: OTTO. This self-driving robot is capable of hauling one metric ton and a half of payload. That’s about 3300 pounds to you and I. Self-driving robots are nothing new to warehouses. In fact, we’ve written about Amazon’s robots, acquired from Kiva Systems, many times before. The difference is that unlike Amazon, these robots do not require navigation devices (RFID, barcodes, etc.). Instead, they have 20-meter lasers front and back (with an option for 50-meter range), and can localize against an existing basemap with an accuracy of about an inch (according to Clearpath). The new robots are in the midst of five pilot programs, the first being a General Electric facility (GE Ventures is a strategic investor in the project). It will be interesting to see how these robots perform in the field, and what impact they may have on the future of autonomous warehouses. And finally, demand for vans on spot market have edged upward. The number of posted loads slipped 0.6% while available capacity declined 2.7% on the spot truckload market during the week ending Sept. 26, according to DAT Solutions, which operates the DAT network of load boards. Van load availability, however, gained 0.6% while the number of posted vans decreased 3.6% compared to the previous week. As a result, the national average van load-to-truck ratio was up 4.4% to 1.7 loads per truck, meaning there were 1.7 available van loads for every truck posted on the DAT network. The national average van rate was unchanged from the previous week at $1.75 per mile.

And finally, demand for vans on spot market have edged upward. The number of posted loads slipped 0.6% while available capacity declined 2.7% on the spot truckload market during the week ending Sept. 26, according to DAT Solutions, which operates the DAT network of load boards. Van load availability, however, gained 0.6% while the number of posted vans decreased 3.6% compared to the previous week. As a result, the national average van load-to-truck ratio was up 4.4% to 1.7 loads per truck, meaning there were 1.7 available van loads for every truck posted on the DAT network. The national average van rate was unchanged from the previous week at $1.75 per mile.